👋 Note: Originally published on Jan 22, 2020 on Medium.

Ethereum began as a blank canvas.

Ethereum is an open, permissionless blockchain that developers can use to create any kind of application they want.

This year, the early strokes laid down on that canvas began to form into a coherent picture.

You don’t have to squint so much to see the direction Ethereum is going. Protocols and applications built on Ethereum are beginning to find product-market fit, quickly building communities of thousands of paying users.

The empty spaces on the canvas are no longer sources of uncertainty or doubt. Instead, they look more like opportunities: what can we build over there?

2019 was the year Ethereum grew more confident. The technical roadmap gained clarity as difficult engineering problems were solved, and the largest developer community in crypto is building applications that people actually pay to use.

This last year, it felt like every big challenge facing the crypto industry as a whole was being addressed primarily by the Ethereum community:

- It’s on Ethereum where decentralized exchanges are solving the problem of trusted third parties, by letting users trade without ever giving up their private keys

- It’s on Ethereum where smart wallets are solving intractable UX challenges, without requiring users give up control over their funds

- It’s on Ethereum where stablecoins like Dai are solving the volatility problems that have made other cryptocurrencies poor payments technology. On Ethereum, peer to peer digital cash isn’t a dream, it’s real — go use it!

Like last year, our goal is to zoom out and show you the bigger picture. This is a summary of the most important developments and trends in Ethereum — the things that we’ll say mattered when we look back in ten years.

In our view, the biggest developments of 2019 were:

- The Ethereum Economy continued to grow. DeFi remains the largest sector within Ethereum, and we saw early signs of growth in gaming & decentralized autonomous organizations (DAOs).

- Ethereum nudged into the mainstream. Major corporations, financial institutions, consumer brands, and even celebrities began actually using Ethereum.

- Ethereum 1.0 improved. A number of projects led to major performance improvements, and a direction was chosen for long-term sustainability.

- Eth2 made progress as an engineering project, and laid the foundation for launching in early 2020.

- Layer 2 made steady progress, with new tech capturing the community’s attention. Rollups and Zero Knowledge technology made the largest strides this year, while other technologies like state channels made steady progress.

1. The Ethereum Economy Grows

In this year’s review, we want to put Ethereum’s adoption into context of the rest of the cryptocurrency industry.

One obviously important metric to use is simply: are people actually paying to use cryptocurrencies and decentralized applications?

Any time someone uses a blockchain like Bitcoin or Ethereum, they pay a small fee which is collected by miners. Here are the total fees paid in 2019:

This graph shows the top 16 blockchains, ranked by fees paid (for obvious reasons, it does not include blockchains where there are no fees). You can see all of the underlying data here.

The reality is that there are only two blockchains with significant use: Bitcoin and Ethereum. As we’ll see in later sections, many individual applications on Ethereum have more paying use than most blockchains with market caps in the billions of dollars.

💰 The Year of Decentralized Finance (Again)

In 2019, Decentralized Finance (DeFi) remained the most significant ecosystem within the Ethereum economy.

The DeFi vision is simple: an alternative worldwide financial system. The internet has made information cheap and universally accessible, and Satoshi made information into money. Every person on earth should be able to access a financial system — payments, savings, lending, investing — through the internet.

Although this system is early, it exists today. If you live in a country with a weak financial system or hyperinflation, DeFi may already be a better alternative than your domestic banks and financial institutions.

DeFi gives us cryptocurrencies that hold a stable value (“stablecoins”), a necessary innovation for any realistic payment use-case. DeFi has enabled thousands of users to earn interest, by lending out their ETH to borrowers. DeFi has enabled the easy creation of assets that automatically execute trading strategies & grow your wealth.

All of this is available today, through a financial system that never closes, is openly auditable and transparent, and where your account can’t be shut down if you work in the wrong industry or have the wrong political views.

This year, one of Ethereum’s under-appreciated virtues came into clearer focus: applications built on Ethereum are interoperable and composable. If you are creating or issuing a new asset onto Ethereum, you can easily “plug in” to a protocol that facilitates asset trades. As David Hoffman puts it, Ethereum is “money legos” that make it easy to create more complex systems. This allows DeFi products to quickly become more useful to users, taking advantage of the extensive infrastructure that has already been built.

While DeFi is still relatively early and risky, the convenient thing about being a financial system is that it comes equipped with tools to help manage risks. The interest rates paid to users who lend their ETH in DeFi have been relatively high, in part because using these platforms introduces risk.

Insurance protocols like Nexus Mutual have sprung up to give users a way to hedge the unavoidable risks of working at the frontier of a new industry. Nexus Mutual launched in July, and in the next 5 months users paid about $11,000 in premiums. That’s greater than the total transaction fees paid to use the privacy cryptocurrency Grin over the same period ($7,600).

📈 How much did DeFi grow in 2019?

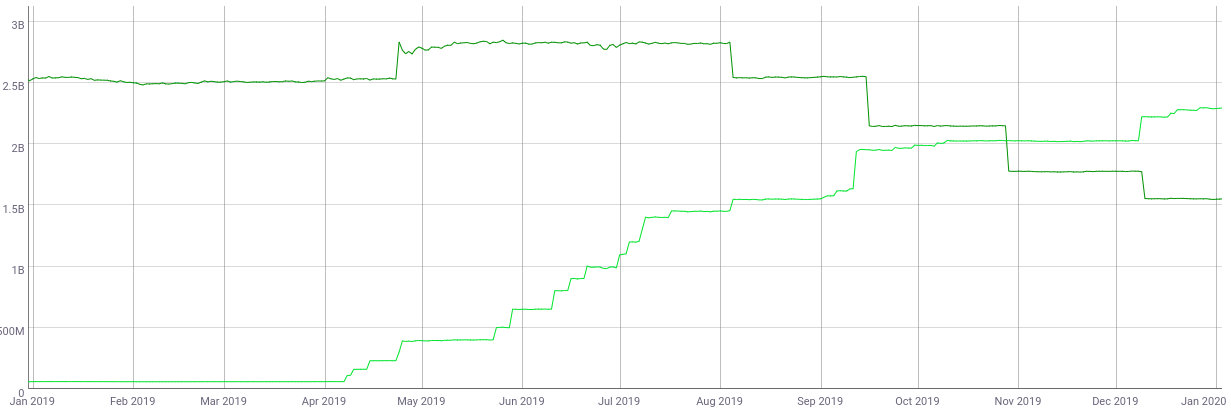

The simplest metric used to track DeFi’s growth is the total value of assets “locked” (TVL) in Ethereum’s DeFi ecosystem. In other words, how much money is currently stored in the smart-contracts that serve as infrastructure for this financial system?

In 2018, this value more than tripled from ~$70 million to $300 million.

In 2019, it more than doubled to $667 million on December 31, 2019:

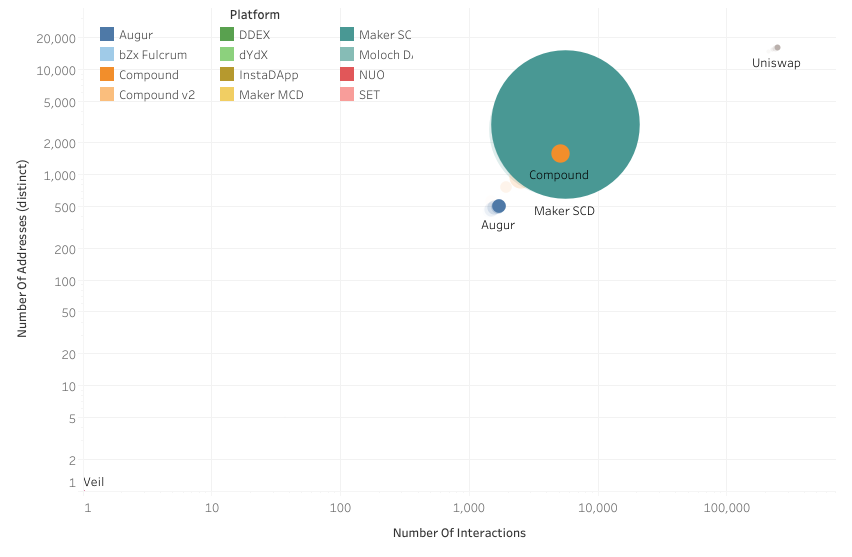

Another way of viewing the growth of the DeFi ecosystem is to visualize not only the total value locked, but the number of accounts using them and how many interactions those accounts have with the application.

At the start of 2019, MakerDAO was the only DeFi protocol with significant funds, a total of 1.86 million ETH (at the time, valued at ~$260.4 million). In the graph below, the size of the circle corresponds to the amount of ETH locked in the protocol:

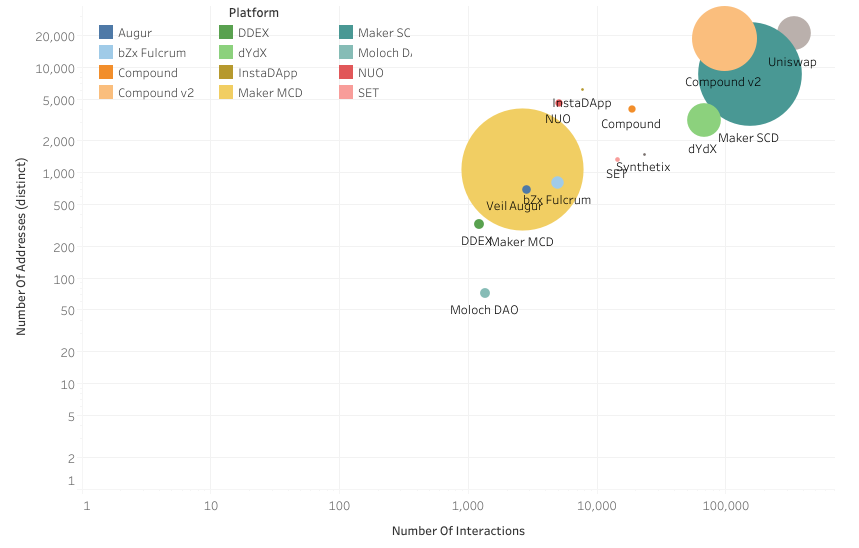

But by the end of 2019, the field was much more diverse:

Compound grew its TVL by 1,000%, from 35,000 ETH to 350,000 ETH, and rapidly grew its number of users. MakerDAO is captured in a moment of transition between the original “single collateral” version of DAI (green circle) to “Multi-collateral” DAI (yellow circle). Both types of DAI have a combined TVL of 2.15 million ETH, an increase of 16%.

🌐 Decentralized Exchanges grow in variety and volume

Decentralized Exchanges (DEXs) are an alternative to centralized cryptocurrency exchanges. DEXs let you trade your assets over the internet without requiring a centralized intermediary like Coinbase, Binance, or Quadriga.

One of the most exciting developments in 2019 was the rise of Uniswap.

Uniswap is a new kind of decentralized exchange. In a “normal” DEX, traders interact with each other — they offer to sell at a price, find a buyer, and then trade directly.

With Uniswap, you trade directly with the Uniswap protocol. The Uniswap protocol itself is the market maker, who sets prices and offers to trade. This is accomplished 100% on-chain, with no off-chain dependencies.

Because Uniswap is built on Ethereum, anyone can use it by calling its contracts. This lets other DeFi protocols utilize Uniswap as a way to bootstrap liquidity for a market, quickly enabling anyone to trade a new asset. Uniswap is one particularly useful “money lego” that has been integrated into many other products and services.

Because Uniswap is built on Ethereum, it is uncensorable. You might be able to take down one particular front-end for Uniswap, but the underlying contracts — the real product itself — remains accessible to anyone with an internet connection.

In 2019, Uniswap went from an average daily volume of $25K to $1.5 million (an increase of +6,000%), and grew its available liquidity from $500K to $25 million (+5,000%).

Over the course of 2019, Uniswap liquidity providers (people who “lock” their assets into the protocol, in order to earn a return for the service of providing liquidity) earned more than $1.2 million in fees.

As a useful comparison, that is greater than the total combined transaction fees paid in 2019 to use Ethereum Classic ($587K), Litecoin ($413K), and Ripple ($179K).

Those three blockchains have a combined marketcap of $13 billion. Uniswap is a team of 4 that raised a $1.8 million seed round in mid-2019.

Also in 2019:

- Beyond Uniswap, DEXs on Ethereum had an impressive year. Total trading on DEX’s built on Ethereum passed $2.3 billion.

- Kyber, one of the largest decentralized exchanges, grew its volume 443% from $70 million to $380 million.

- 0x ended the year with $254 million in volume, and the number of trades increased 27% — a year of focusing on liquidity and R&D.

- We saw the rise of DEX aggregators like Totle, dex.ag and 1inch.exchange. These are services which allow users to find the best price across DEXs.

🏦 Lending Services

One of the most significant developments in Ethereum’s DeFi ecosystem was the rapid growth of lending services.

These applications let users lock their cryptocurrency into smart contracts, where other users can borrow it, paying you interest. In 2019, more than $600 million in loans were originated on Ethereum. That is more than double the total value of all payday loans made in Washington state in 2017 ($248 million).

For instance, right now you can take any DAI you have, and start earning 5.9% interest annually by lending it through the Compound lending protocol. In 2019, Compound grew its TVL from $20 million to $91 million.

Or, you could lock some of your ETH into the MakerDAO protocol, as collateral to take out a loan of DAI (which you could then lend on Compound, if you wanted).

In 2019, users paid $5.5 million in fees to the MakerDAO protocol, a total that is greater than the sum of all transaction fees paid on every blockchain other than Bitcoin and Ethereum.

💵 Stablecoins

Stablecoins fulfill the original vision of cryptocurrency as “peer to peer digital cash” — a useful means of making cheap, fast payments over the internet. A digital dollar you can use to make payments, receive your salary, and that won’t lose its value overnight in the volatile cryptocurrency markets.

Virtually all stablecoins are built on Ethereum. This year, Ethereum gained even greater dominance as the default platform for stablecoins, as Tether — the oldest and largest stablecoin — moved a majority of its outstanding supply over to Ethereum, transitioning off the (Bitcoin based) Omni protocol.

In 2019, Tether issued approximately $ 2.3 billion onto Ethereum, with more than $1 billion of that total directly coming at the expense of Bitcoin’s Omni. This was the largest migration of assets from one blockchain to another in history.

MakerDAO, the protocol which supports the Dai stablecoin (covered extensively in Year in Ethereum 2018), went through a major upgrade. While originally DAI could only use ETH as the “single collateral” available to issue new DAI, in November MakerDAO successfully launched “Multi collateral DAI” which makes it possible to use many assets on Ethereum in the system.

💥 A Cambrian explosion of Ethereum-based assets

One major new trend in DeFi is the expansion of products and protocols that facilitate the use of synthetic assets. By “synthetic asset” we simply mean an asset that is designed to have specific characteristics, often imitating the profile of other assets.

The programmability and interoperability of assets on Ethereum makes this easy. Using Ethereum smart-contracts, developers have created assets that track the value of other cryptocurrencies, automatically implement specific trading strategies, or create custom derivatives.

Set protocol launched TokenSets in April, a suite of products that allow anyone to purchase an ERC-20 that then implements a specific trading strategy. For instance, you might buy $1,000 worth of the “ETH 20 Day MA Crossover” set, which rebalances between ETH and the USDC stablecoin, depending on a specific market indicator. The goal is that when ETH is rising, this TokenSet is mostly ETH, and when ETH is falling, it swaps into a stablecoin to avoid losses.

Universal Market Access (UMA) introduced a service that lets anyone create synthetic tokens that track the price of real-world assets like stocks, or really anything at all that you have a price feed for. At the ETHBoston hackathon, hackers used UMA to create a synthetic asset that tracks whether DAI deviates from its dollar peg, resulting in a massive payoff if the peg breaks. At ETHWaterloo, the UMA team created a synthetic asset that tracked the amount of human fesces sightings in San Francisco, which they promptly integrated into a fork of Uniswap so people could trade it on testnet.

Synthetix launched their “synths” product, which are ERC-20s that track the value of major currencies, commodities, or indices. Notably, Synthetix began trying to implement their protocol on EOS, decided it was a mistake, and have doubled down on building on Ethereum.

In 2019, users paid approximately $3.5 million in fees to use Synthetix, a total that is greater than the sum of all transaction fees paid on every blockchain other than Bitcoin and Ethereum.

Also in 2019:

- Efforts to make Bitcoin useable on Ethereum gained momentum. Kyber, Bitgo, and Republic launched wBTC, an ERC-20 backed by real Bitcoin, stored with trusted custodians. In August, Keep & Summa announced their plans for “trustless BTC” (tBTC), which required no central counterparty to custody the BTC. Launched is planned for 2020.

- RealT tokenized the legal ownership of several houses in Detroit — starting with 9932 Marlowe. Owners of these tokens have access to liquidity through Uniswap, where they can always find a counterparty to buy out their stake in the home.

- Compound — already mentioned above in the lending section — launched cDai, a token that accrues interest. Products like cDai are collapsing the distinction between a “lending service you use” and “an asset you buy”.

- Many synthetic assets depend on some kind of Oracle to report information. “Trustless” oracles are unsolved, and remain one of the hard problems in the cryptocurrency space.

👾 Ethereum’s gaming sector grows

In 2019, Ethereum’s gaming ecosystem showed early signs of growth.

One of the standout examples is Gods Unchained: a turn-based, collectible card game similar to Blizzard’s Hearthstone. The difference is that Gods Unchained cards are assets on Ethereum: they can be bought, sold, traded over DEXs, or even someday used as collateral.

In 2018, they sold $4 million worth of cards to the market, and this year they began “activating” those cards to be used in the game. This led to the largest number of transfers of “non-fungible” tokens (ERC-721s) in history:

In November, GU enabled open trading of the cards. Within a few days, more than $220K worth of cards had been traded on OpenSea, a popular marketplace for NFTs.

The other notable gaming launch was PoolTogether.

PoolTogether is a no-loss lottery system, made possible by Ethereum. It’s simple: players deposit DAI into a program running on Ethereum. That pool of money earns interest over time, by automatically lending it out on Compound. Then, at the end of the period, one player wins the earned interest (as of this writing: $688 every week). It is “no loss” because if you don’t win, you haven’t lost the price of your “ticket” since you can just withdraw your funds.

PoolTogether launched in June, and in the next six months its users won a total of $3,594. Over the same six month period, Tezos validators earned transaction fees totalling $3,745.

PoolTogether is especially notable as an indicator of a larger trend: financial applications that look like games, and games that look like finance. There has always been a space where these two realms collide — WoW, EVE Online, casinos, the stock market — but Ethereum lets us collapse the distinction entirely. Expect to see more entrants to this new category in 2020.

Also in 2019:

- Skyweaver, an Ethereum-based card game launched their Beta in June and raised $3.75 million from investors.

- Decentraland, a virtual world where property exists as an asset on Ethereum, readies for its public launch in early 2020.

- Cryptokitties — the first breakout game on Ethereum — maintained its dominance, as Cryptokitties were still the most-transferred NFT on Ethereum.

👹 Decentralized Autonomous Organizations

Since the early days of Ethereum, people have dreamed of creating Decentralized Autonomous Organizations, or DAOs.

The idea is simple: Ethereum lets us write un-censorable code that executes on a distributed, decentralized platform. We could create a program that holds funds, and defines a governance process used to determine how to manage those funds. For instance, by defining a voting process.

Since the painful “The DAO” fork in 2016, the idea has been haunted by a mixed legacy. But in 2019, new projects revived interest in DAOs.

While 2019 did not become the “Year of the DAOs”, it did have at least a few “Months of Moloch”. MolochDAO, which launched in February 2019, is aimed at funding important public goods in the Ethereum ecosystem. Using money donated from several sources (like the Ethereum Foundation, Vitalik, Joe Lubin, and ConsenSys), the members of the MolochDAO vote on which projects to fund.

This simple model ended up being the DAO project that most captured the Ethereum community’s attention, and was echoed by several other efforts like MetaCartel and MarketingDAO. Ross Campbell began an effort to launch “LAOs”, or “Legal DAOs” that interoperate with traditional legal systems, influenced by the MolochDAO framework.

In another notable example of the value of Ethereum’s composable nature, Saint Fame — a “decentralized fashion house” DAO — launched their first product in December.

Saint fame issues tokens on Uniswap, which can later be redeemed for a specific product: a designer t-shirt. Trading the tokens openly on Uniswap lets the price of the t-shirt rise and fall in response to demand. Members of the DAO will vote on how funds are used to create new designs, which can then be sold through the same mechanism.

Saint Fame is built using Aragon — a comprehensive framework and toolkit for DAOs. Aragon itself saw early signs of adoption, and by the end of 2019 more than 900 DAOs had been created by the framework.

2. Ethereum nudges into the mainstream

In September, NBA player Spencer Dinwiddie announced plans to “tokenize” his contract. He would sell 90 Ethereum-based tokens, which would give the holder a portion of Spencer’s future contract value, plus interest. In exchange, he would receive $13.5 million out of his $34 million contract up-front.

The NBA initially opposed the move, claiming it breached Spencer’s contract with the league. But over the next few months, the plan was back on, set to launch in January 2020.

The most astonishing thing about this story is that in 2019, it didn’t seem out of the ordinary. If you had speculated in 2015 that within a few years an NBA player would be actually using Ethereum as a platform for financial innovation, no one would have taken you seriously.

But this year it happened — along with a lot of other small moves towards the mainstream:

- The Sacramento Kings launched a rewards-token built on Ethereum.

- Star Trek announced a series of collectible iconic ships, which will be issued as NFTs on Ethereum.

- Opera, the 6th largest browser in the world, added native support for Ethereum at the end of 2018, and in 2019 launched a desktop browser complete with a “Dapp store”.

- Samsung released a developer platform built for Ethereum, and announced a new phone with a built-in Ethereum wallet.

- Ethereum’s DeFi ecosystem was covered in Bloomberg

- Gridplus — an energy company built on Ethereum — went live in February, and now serves electricity customers in Texas

Meanwhile in the enterprise world, the lines started to blur between “Enterprise Blockchain” and “Mainnet Ethereum”.

Mainstream enterprise corporations have realized that spinning up a private or consortium chain isn’t that different from a siloed, centralized database. But they’ve started to pursue an interest in mainnet Ethereum, which offers an open platform backed with billions of dollars of economic security.

One of the strongest proponents of mainnet for enterprise has been EY, who continued their work on “Nightfall”. Nightfall is a project that aims to enable enterprise to use Ethereum mainnet, while ensuring that the transactions are private and scalable — addressing two of the major concerns that limit enterprise use of Ethereum today. In December, EY launched v3 of Nightfall, bringing the transaction cost down to pennies instead of dollars.

Meanwhile, Microsoft continued its deep involvement with the Ethereum ecosystem. In May, Microsoft released the Azure Blockchain Development Kit, specifically to support Ethereum development. Visual Studio, Microsoft’s popular IDE, now supports Ethereum through an extension, fully integrated with Truffle. In June, they announced VeriSol, a formal verification tool for Ethereum.

In October, Microsoft joined with the Enterprise Ethereum Alliance to work on a tokenized incentive system for use within enterprise consortiums. And in November, Microsoft launched Azure Blockchain Tokens, a service that lets enterprises issue their own tokens onto Ethereum.

Many of these developments — in both consumer and enterprise contexts — might seem small. But together they paint a clear picture: even as general interest in cryptocurrency has slowed and flattened, Ethereum continues to reach outside the cryptocurrency industry, and is seeing early signs of adoption beyond the core community.

Also in 2019:

- HyperLedger Besu becomes first public-chain client in Hyperledger.

- Cloudflare launched an Ethereum Gateway.

- JP Morgan announced plans for their JPM Coin bank-backed cryptocurrency. In May, they added to Quorum an implementation of the Zether confidential payments protocol.

- Banco Santander settled a $20mm bond on mainnet Ethereum (you can see the transactions here).

- Many, many other examples — too many to list here.

3. Ethereum 1.0 performance & sustainability

Every application we covered above — from the hundreds of millions of dollars in DeFi protocols, to trading cards, to enterprise applications — runs on today’s Ethereum protocol and today’s Ethereum clients.

This year, “Ethereum 1.0” and the clients that support it received some of the most significant upgrades since Ethereum’s homestead release in 2016. These changes began to address state growth, client sync times, client disk IO, transaction throughput, and issuance. In 2019, more EIPs were deployed than in any other year.

🏆 Geth

Geth, Ethereum’s dominant client, received major upgrades this year. In July the Geth team released v1.9.0, which included major performance improvements and many new features. This year, the Geth team reduced the time to fast-sync a full node by half to ~ 4 hours, and implemented a 10x reduction in disk IO.

The Geth team deserves extraordinary credit for continuously improving the majority client software powering Ethereum. While this work may not always receive the attention of a new breakout application or area of theoretical research, it is the work that makes Ethereum possible.

Have you thanked your Geth maintainers today?

⚙️ ETH 1.X

At Devcon4 in November 2018, a group of core developers began to talk informally about how to make Ethereum 1.0 more performant in state size, sync times, and disk IO. While the long-term goal is a migration to Eth2, Ethereum must remain sustainable until that time.

In the months after Devcon, this initiative became known as “ETH 1.X”. While many took this as an opportunity to push for a wide variety of ideas on how to change the EVM, fundamentally the core goal has always been sustainability through ideas like state rent, stateless clients, or repricing gas costs.

The results have been major improvements to Ethereum 1.0 across the board.

Ethereum’s maximum throughput increased from ~25 transactions per second, to ~38. This was achieved by increasing the block limit to 10mm gas, while block times were reduced to 13 seconds after the Istanbul hard-fork. EIP-2028 contributed to this improvement as well, by reducing the gas cost of a single byte in a tx input from 68 gas to 16 gas.

Client optimizations to Parity suggested by Alexey Akhunov made it possible to increase the block limit without a corresponding increase in the uncle rate. As a result, uncle rates plummeted in 2019.

Ethereum’s issuance of new ETH fell in 2019. The Constantinople hard-fork reduced issuance per block from 3 ETH to 2 ETH. Further, the decline in uncle rates above also reduced issuance, since uncle blocks win partial rewards.

As a result, Bitcoin and Ethereum now have similar issuance rates, with ETH’s planned issuance rate to drop again when the network is entirely proof of stake:

To address long-term sustainability, 2019 saw major advances in research towards a “stateless” model for Eth1. Other approaches that were considered at the beginning of the year, like state rent, have been de-prioritized.

The goal of the stateless model is to reduce the amount of state-data that must be stored by each node. Using simple techniques like Merkel trees, we can provide a “block witness” to prove that a specific piece of data is in a specific block, without requiring the client to hold that block’s state data. Many nodes will still hold full state, but using these techniques we can allow some nodes to store less data.

One related project is Beam Sync, which uses block witnesses to cut sync time to a matter of minutes, while completing a “full” sync in the background. Beyond that, other types of “semi-stateless” clients will be introduced as work progresses.

4. Eth2 is (almost) here.

Ethereum’s vision has always been a scalable, proof-of-stake blockchain. It has been clear since the early days of cryptocurrency that despite being a technological leap forward, proof of work is deeply flawed.

Even optimistic estimates of Bitcoin’s energy use put it as roughly comparable to the total energy used by countries like Portugal or New Zealand. Migrating to proof of stake will eliminate this wasteful energy use, and allow Ethereum to grow over decades without radically increasing the world’s energy consumption.

While the broad outlines of Ethereum’s migration to proof of stake were clear even in 2015, filling in the details has taken careful, difficult work.

Ethereum’s migration to proof of stake — known as Eth2 — has taken longer than many expected. After multiple years of R&D, 2018 saw the project transition from a research topic to an engineering challenge. In 2019, multiple independent teams worked together to build the software necessary to launch the first phase of Eth2. There is now little doubt that Eth2 will enter production in 2020.

Like any good open-source project, Eth2 is being built in the open. This process can seem messy to those who aren’t familiar with the “bazaar” model of open-source software development, or who are more familiar with cryptocurrencies controlled by a single client team.

Eth2 is a large project that will be rolled out in phases over multiple years. The first phase — Phase 0 — is expected to launch in Q2 2020. This involves launching the Beacon Chain, which serves as the “backbone” of Eth2. Phase 1 then introduces the Shard chains, which are secured by the underlying Beacon chain. In Phase 2, the system comes together into a functional whole. Shard chains become useable for transactions and smart contracts, and all of the core features familiar to users of Ethereum today.

At the beginning of the year, 9 independent teams were inspired to begin work on implementing Phase 0’s beacon chain. By the end of the year, Eth2 is beginning to see mature testnets.

These began in the summer as short-lived private testnets from a single team, and by September multiple clients were able to interact on a shared testnet. Key to this progress was Joe Delong’s push for a weeklong networking lock-in in Skeleton Lake, Ontario, where Eth2 implementer teams achieved interoperability between their clients and established networking standards. By December, this progress had enabled longer-lived public testnets between multiple teams. You can even view these testnets on public block explorers like Etherscan.

As Eth2 came into clearer view, the broader developer community was able to offer feedback — and criticism — that led to adjustments. Specifically, shortly after Devcon, Vitalik published several notes proposing changes to Phase 1 that would reduce the complexity of interaction between shards.

Discussion remains active on the best approaches to implement Phase 1 and Phase 2, as well as how best to migrate the existing Ethereum blockchain into Eth 2. Currently there are proposals being debated that would have Eth1 be the first shard of Eth2, which would take place between Phases 1 & 2. There is also active debate around finalizing the current Eth1 proof-of-work chain with Eth2´s beacon chain, which would enable a much earlier reduction of ETH issuance.

Meanwhile, Phase 1’s data availability will allow Layer 2 solutions like rollups and state channels to blossom. For example, the potential throughput of rollups (which can already facilitate 2,000–3,000 tps on Eth1) will increase by about 100x.

Eth2 is coming — get ready to stake in 2020.

5. Layer 2 and off-chain tech

The idea behind all Layer 2 technology is that we can perform expensive computation “off chain”, while still retaining Ethereum’s characteristic security guarantees. This “second layer” can process transactions or computation much faster than Ethereum mainchain, leading to a more scalable network overall.

In late 2018, Barry Whitehat, proposed ZK rollup. The basic idea is that we perform many transactions *off-chain, *and “bundle” them together. This “rolled up” group of transactions are then verified using succinct Zero-Knowledge Proofs (SNARKs), which confirms that each transaction is correctly signed by owners, preventing any invalid or manipulated transactions.

In early 2019, multiple streams of work adapted this idea in a new direction. In June, John Adler & Mikerah published their work on “Minimal Viable Merged Consensus”, and in parallel Plasma Group published their work on the “Optimistic Virtual Machine” in July.

Eventually, the research community settled on “Optimistic rollups” to describe this category of technique, which bore similarities to an idea Vitalik initially called “shadowchains” in a 2014 blog post. Vitalik helpfully summed up this area of research in an August blogpost.

Optimistic rollups use a similar technique of “bundling” transactions as ZK rollups, but use a different mechanism to “prove” them. Instead of using SNARKs, Optimistic Rollups use a cryptoeconomic mechanism that lets the system “Optimistically” assume there are no invalid transactions, while still catching, preventing, and punishing (slashing a deposit) those who try.

In October, Plasma Group shipped a demo that used an Optimistic Rollup to deliver a lightning-fast version of Uniswap at Devcon called Unipig.

ZK Rollup and Optimistic Rollup have different advantages and disadvantages. Optimistic rollups are easier to implement in the near-term, and flexible enough to be used with different applications. ZK Rollup, however, has more potential in the long term, but is more specialized due to its use of zero knowledge proofs, and will require more R&D before it is useful for a wide variety of applications.

Meanwhile, State Channels entered into a far less sexy, but no less important, phase of their development. With no outstanding research problems, several teams worked towards implementing a viable framework that applications could use to support channelized apps.

In July, the primary state channels teams met at ETHNewYork to discuss unifying standards and ensuring interoperability. This led to the announcement of a single, unified specification, simply called State Channels. Counterfactual and Magmo merged their engineering teams, replacing their own brands with the new joint project, and continued to make engineering progress.

State channels projects launched onto mainnet this year. In March, Connext — a micropayments platform — launched the Dai Card, a simple browser-based payment system running built on channels. In September, Connext launched v2.0 of their platform onto mainnet, built on top of the now-unified State Channels codebase.

In July, Celer launched their mainnet alpha. By October, CelerX mobile app was supporting 60k monthly active users.

Adex, with a custom implementation of their own payment channels framework, quietly built a significant payment channels network, settling more than 9 million transactions in a 2 month period over the summer.

Starkdex — a project between Starkware and 0x — launched a PoC in June. In October, they released OpenZKP, an open source rust implementation of ZKPs. In October, Starkware announced their plans to launch the first STARK powered Dex in collaboration with Deversifi, in early 2020.

What did it all mean?

This post isn’t comprehensive. How could it be? There’s too much happening on Ethereum to keep track of, even when you write a weekly newsletter about it.

A few other items that deserve note:

- Smart wallets launched and gained traction. Smart wallets use smart contracts to implement access and control logic, making the wallet more useful. For instance, this enables multi-factor authentication, “batching” of transactions for ease of use, and better recovery methods in case of lost keys. Three notable entrants in this category are Argent, Dharma, and Gnosis Safe.

- Big ethereum wallets continued to get bigger. Metamask exceeded 1 million installs on the Chrome store, and launched a mobile version. Brave, an Ethereum-based browser and wallet, surpassed 10 million monthly active users, and reached more than 350,000 “publishers” for its micropayment platform as of December.

- Prediction markets made steady progress. Augur doubled its open interest from $1.3 million to $2.7 million, Gnosis’ Sight prediction market launched into Alpha, and Numerai’s Erasure protocol went live on mainnet.

- Ethereum Name Service (ENS) launched the new permanent registrar, made ENS names NFT compatible, and saw users pay $350K in fees across its two registrar contracts. That’s roughly equivalent to the total fees paid to use Dash, Monero, NEO, Bitcoin Cash, and Bitcoin SV combined in 2019.

- The Ethereum community expanded its ability to fund public goods. MolochDAO launched, Gitcoin Grants captured the community’s attention, and the Ethereum Foundation’s grant program was reborn as Ecosystem Support.

- Ethereum.org got a reboot, and the Ethereum community has translated it into 20 languages, while the site has more than 100 contributors

- Oh, and ETH is money.

If you only pay attention to generic crypto news, you might think 2019 was a disappointing year. The market drifted sideways, new basechain protocol launches uniformly disappointed, and the hyped-up blockchain headlines disappeared from the news. It might seem like crypto is dying.

But if you’ve read this far, it should be easy to see why the Ethereum community hasn’t shared this sentiment.

In 2019, it’s clear that there’s enough real activity at the application layer to give us some confidence that Ethereum is growing in the right directions. The work being done at the protocol level means that Eth1 can be sustainable in the medium-term, and steady tangible progress on Eth 2 builds confidence that Ethereum could someday scale to billions of users. It’s been a harsh winter, but Ethereum kept on building straight through it.

Crypto is dead? Long live Ethereum.

— Josh Stark (ETHGlobal, L4, Ethereum Foundation) & Evan Van Ness (Venture Partner at ConsenSys Labs, Week in Ethereum News)

Thank you to Jinglan Wang, Danny Ryan, Hayden Adams, Alex Xu, Hugh Karp, David Hoffman, James Hancock, Alexey Akhunov, and many others for their contribution to this piece.