Author: PSE Trading Analyst @Yuki

Since the transition of Ethereum to Proof of Stake (PoS), the emergence of LSDFi (Liquidity Staking Derivative Finance) has presented a new and intriguing avenue in the market. LSDFi has drawn attention for its innovative approach to yield-bearing tokens based on liquidity staking. However, as the staking rate of ETH increases and the yield on staking decreases, squeezing market space, the growth of LSDFi has stalled.

Looking back, we have witnessed three phases in the development of the LSDFi track: from the competition among liquidity staking protocols to LST (Liquidity Staking Tokens) becoming a new consensus asset in DeFi, and then to the diversification and wide application of LST. Currently, we are facing a clear developmental dilemma. This article aims to clarify the current state of the LSDFi track with data and explore the future direction of LSDFi through analysis of specific projects.

1. The Current State of the LSDFi Track from a Data Perspective

1.1 The period of growth dividends has passed, with stagnation in development and a decrease in yield rates leading to capital flight.

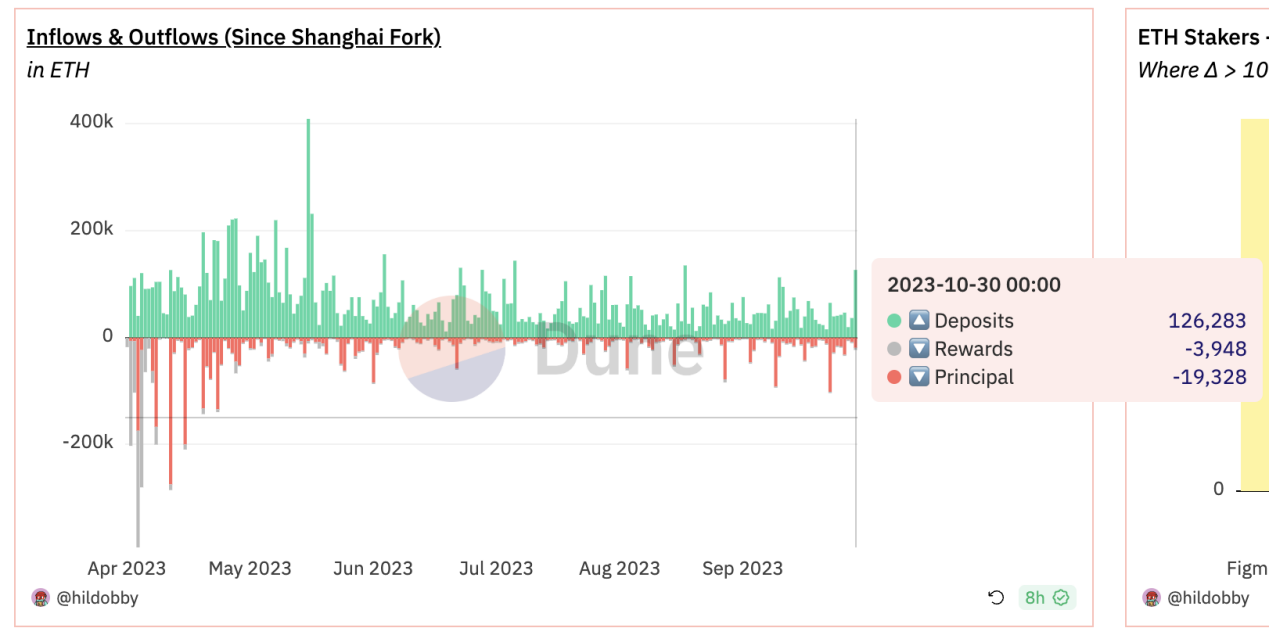

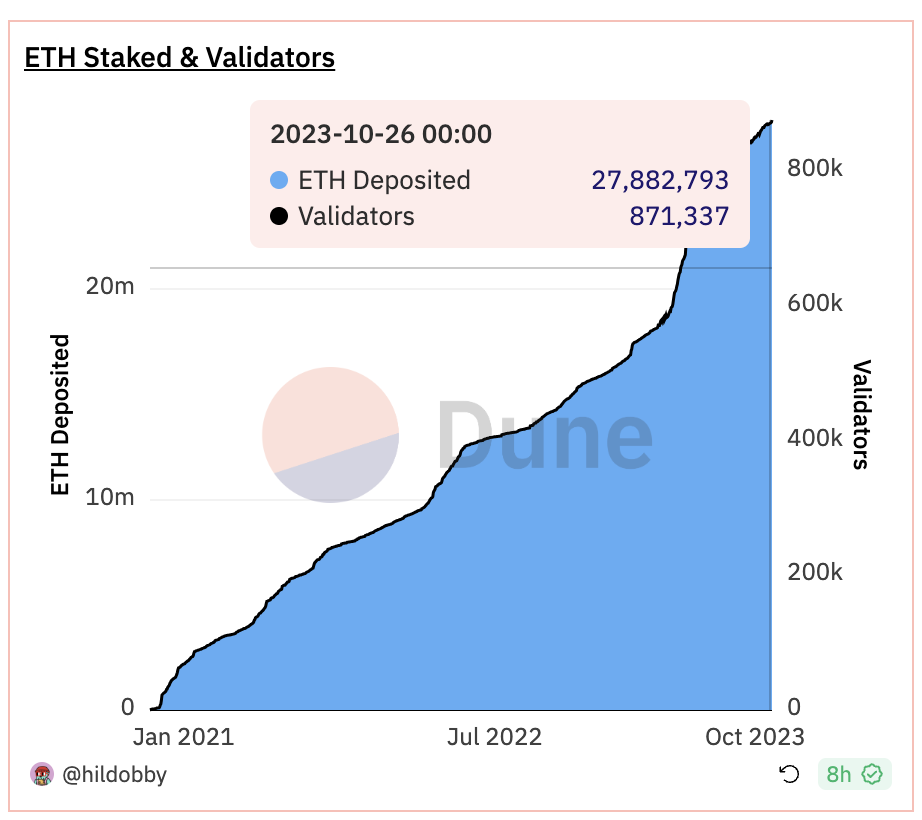

According to data from Dune Analytics, the number of ETH net staked is flattening, and the queue of validators waiting to enter is decreasing, indicating the end of aggressive staking growth. Correspondingly, the total TVL (Total Value Locked) of the LSDFi track has been slowing down since September 26 of this year, with negative growth appearing. Without paradigmatic innovation, it is foreseeable that there won't be significant growth in the LSDFi track for some time.

There are two possible reasons for this situation. On one hand, the internal staking growth within the Ethereum ecosystem is weak, and the increase in the staking rate has led to a decline in staking yield (with a base rate of just over 3%), causing LSDFi protocols to hit a yield bottleneck, decreasing the track’s attractiveness to capital, leading to capital outflows. On the other hand, the external environment, especially the rising yield of US Treasury bonds in the high-interest-rate environment in the United States, has created a siphon effect on capital from the crypto industry, with LSDFi funds fleeing to higher-yielding US bonds and DeFi-based bond derivatives.

1.2 Homogenization of projects is severe, with competition but a lack of innovation.

To date in DeFi, lending and stablecoins still shine as foundational components that sustain the system. In the operation of LST, lending and stablecoins are also the most basic and feasible modes of operation. Based on the yield-bearing nature of LST, LSDFi track projects can generally be divided into two categories:

— LST as collateral for lending protocols or stablecoin protocols (represented by Lybra, Prisma, Raft);

— Separation of principal and interest of LST (represented by Pendle).

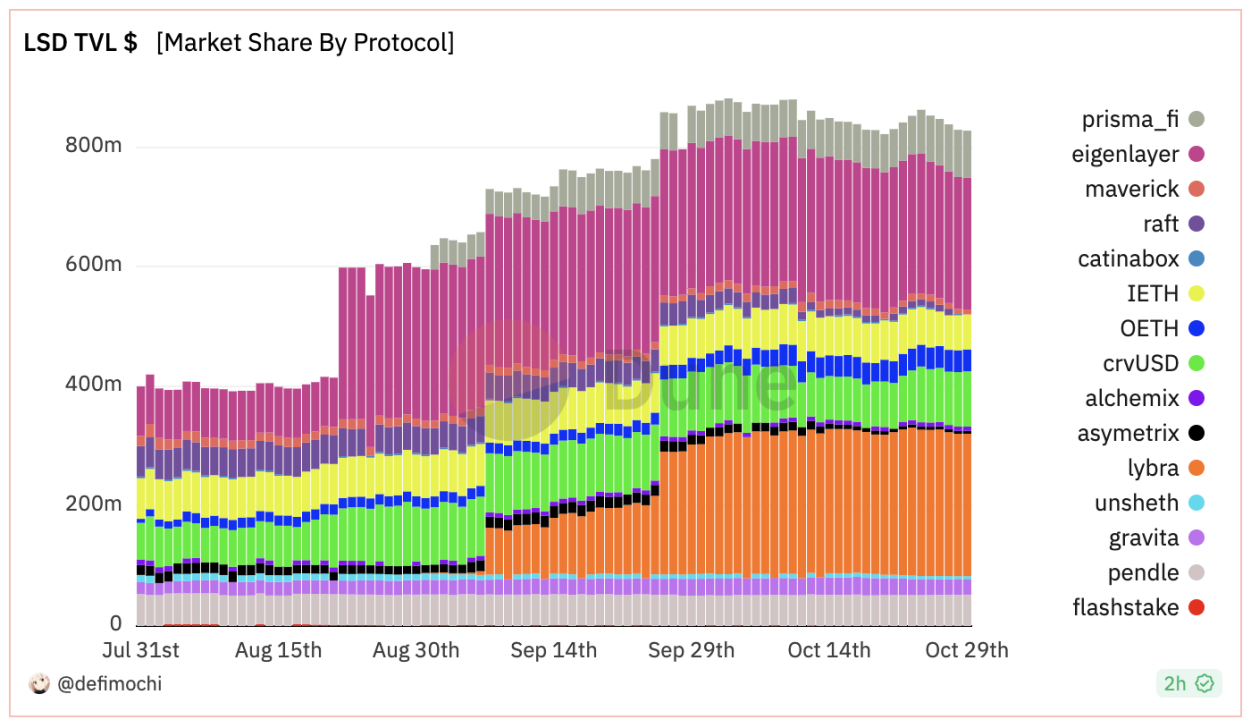

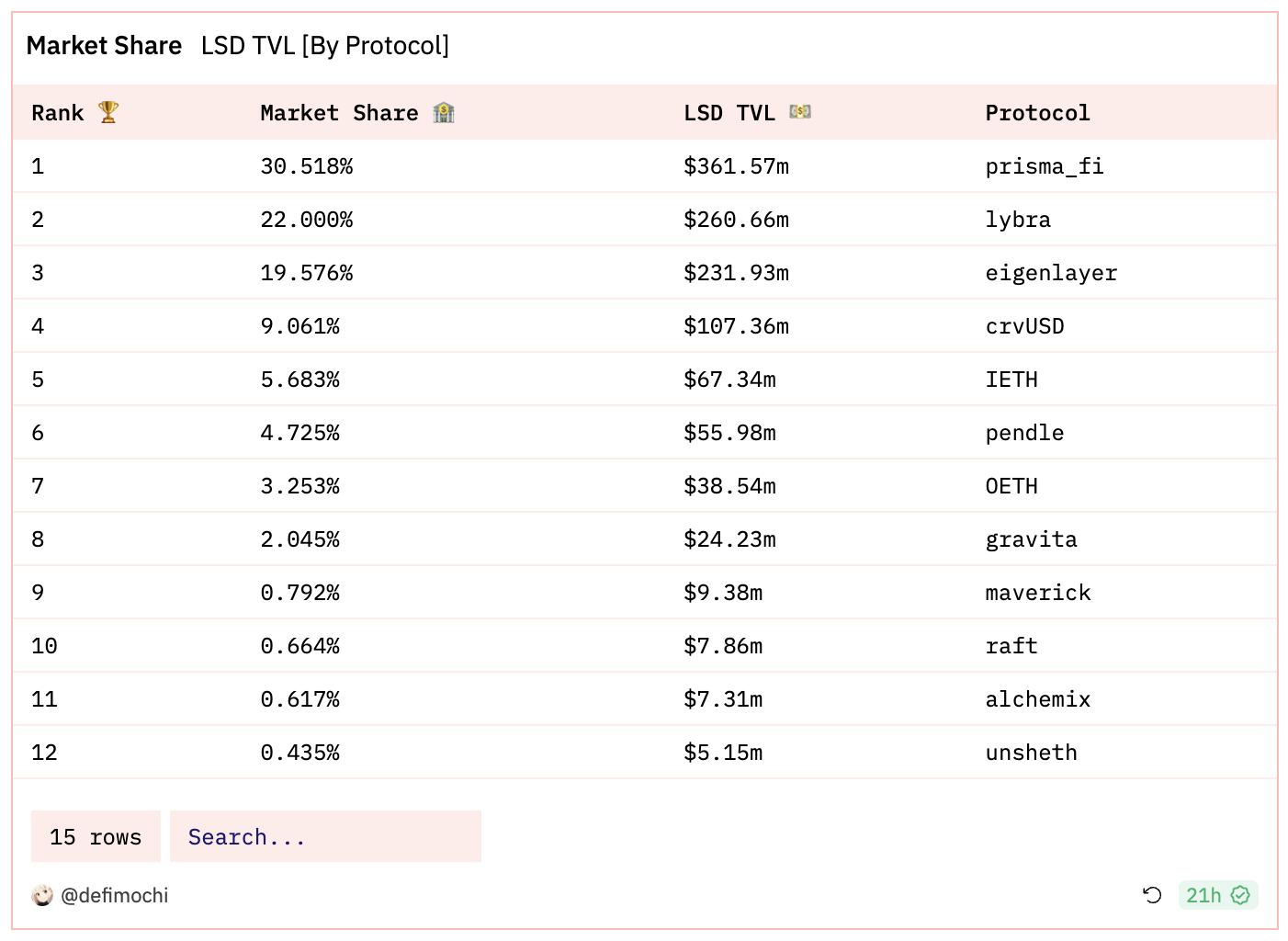

Data from Dune Analytics shows that among the top 12 projects by TVL in the LSDFi track, five are based on LST stablecoin protocols. Their mechanisms are nearly identical: users use LST as collateral to mint or lend out stablecoins; when the price of the collateral falls, it gets liquidated. The few differences lie in various stablecoins, Loan-to-Value (LTV) ratios, and supported collaterals.

After the collapse of Terra and the forced delisting of BUSD due to regulatory risks, the stablecoin market has seen many gaps that need filling. The emergence of yield-bearing LSTs could contribute more decentralized options to the stablecoin market. However, after the initial surge, the overall innovation within the track has been weak, revolving around internal competition over LTV, collateral types, and stablecoin yields (which largely rely on project token subsidies and are fundamentally unsustainable). Latecomers without distinctive features challenging incumbents signify the end of their project upon launch.

Pendle stands out in the LSDFi track with its fixed-income products, which naturally suit yield-bearing LSTs (for example, stETH can be split into ETH and staking yield parts). This is why Pendle has reemerged at the center of the market following Ethereum's transition to PoS. Currently, Pendle is holding its market share with product iterations, with no strong competitor of the same type emerging yet.

1.3 Top Projects Lack Pricing Power, Long-Term Growth Not Guaranteed

In the DeFi sector, we can regard Aave as the leader in lending protocols, Curve as the leader in stablecoin DEXs, and Lido as the leader in Ethereum liquidity staking services. These projects have achieved pricing power in their respective fields. Here, the pricing power I refer to is the barrier effect formed by "monopoly + necessity", which creates a certain monopoly and brand effect in the market's essential services (significantly leading in market share).

What does having pricing power mean? I believe it signifies at least two advantages: one is an excellent business model, and the other is guaranteed long-term growth. In summary, the barriers with pricing power are the real barriers.

However, looking at the various projects on the LSDFi track, even the market-leading Lybra Finance has not formed its pricing power barrier. In its V1 phase, Lybra stood out from a host of LSD stablecoin protocols with a yield far exceeding the base staking yield of Ethereum (8%+), attracting a significant amount of TVL. However, the V2 upgrade did not bring effective growth to Lybra; instead, it was continuously squeezed for market share by later projects like Prisma and Eigenlayer.

The inability of leading projects in the track to possess their pricing power is fundamentally due to: first, the technical difficulty of the project as a protocol layer is not high, not to mention many LSD stablecoin protocols are directly forked from Liquity, meaning "low technical threshold" implies that competition will definitely be fierce; secondly, LSDFi projects are not issuers of LST, essentially relying on ETH's pricing power (staking yield) to redistribute liquidity; lastly, the differences between projects are minimal, and market share is often influenced by protocol yield rates, while leading projects have not formed their own ecosystem to establish absolute pricing power within it.

The lack of pricing power actually means that the current prosperity may all be temporary, and no one has found the key to long-term growth security.

1.4 Token Subsidized Yield Rates are Unsustainable, Stablecoin Liquidity is Sluggish

Previously, LSDFi projects quickly gathered a large TVL by offering high yields, but upon closer examination, we'll find these high yields are subsidized by the project tokens, which leads to the premature depletion of the governance token's value, making high yields unsustainable.

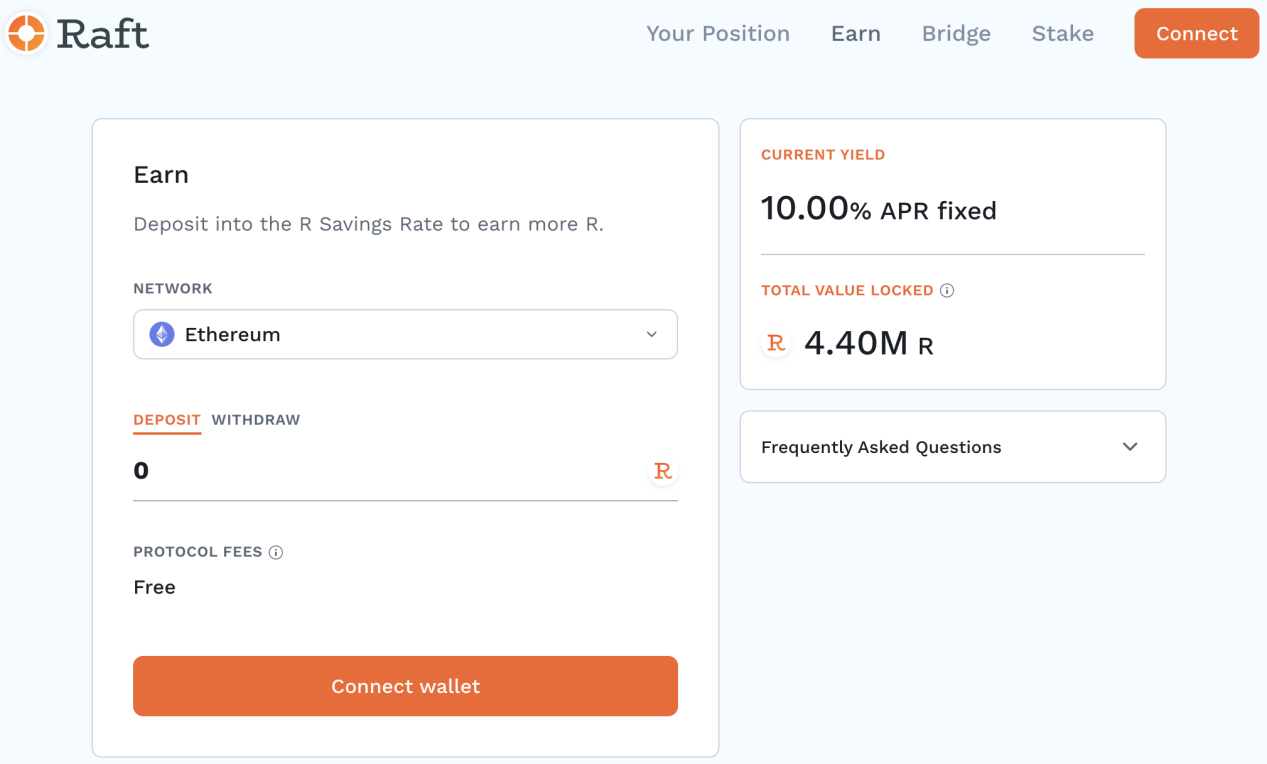

Take Raft as an example, Raft launched a Savings Module with V2, attracting depositors with a 10% fixed APR for $R holders. However, there was no detailed disclosure about the source of this 10% interest (officially explained as subsidized by protocol income). Looking at the whole DeFi sector, there are very few projects that can offer a 10% low-risk rate, which raises doubts about whether the project team is creating $R out of thin air to craft this seemingly beautiful APR myth.

It is worth noting that Raft's collateral borrowing cost (interest rate) is 3.5%, which means users who mint $R and deposit it into RSM can achieve at least a 6.5% arbitrage.

For decentralized stablecoins, liquidity is the biggest factor affecting their scale of development. Liquity did not expand its scale or break through in the last bull market precisely because its liquidity could not meet user demands. And currently, DAI indeed has the best liquidity among decentralized stablecoins. Similarly, most of the current LSD stablecoins are also facing liquidity issues; their self-issued stablecoins lack depth and diversified use cases, and there isn't enough real user demand.

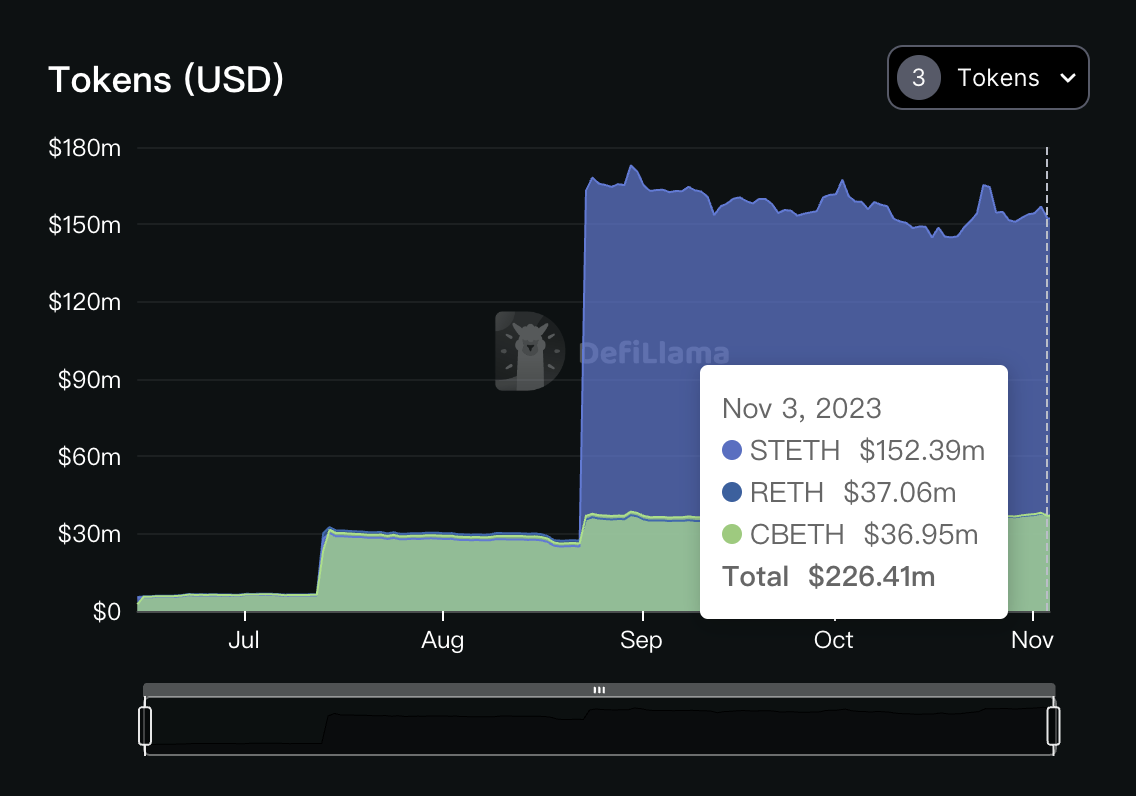

Take Lybra's eUSD as an example; its current scale is 108M, but the deepest liquidity pool is the peUSD pool on the Arbitrum chain (peUSD is the cross-chain version of eUSD). The depth of the eUSD-USDC pool on Curve is only 207k, indicating that the exchange between eUSD and centralized stablecoins is very inconvenient and may affect user experience to some extent.

2. Looking at specific projects, searching for breakthroughs in the development dilemma of LSDFi

Although the LSDFi sector as a whole is in a developmental bottleneck, there are still projects actively seeking change, from which we may gain insights and inspirations to break through these challenges.

2.1 Develop ecosystems, compensate for economic model deficiencies, establish pricing power: Take Pendle and Lybra V2 as examples

At present, LSDFi projects share a seemingly insurmountable issue: subsidizing user yields with governance tokens, leading to continuous dilution of their value, eventually reducing them to worthless mined coins.

A viable and exemplary solution is to develop their own ecosystems, leveraging the strength of ecosystem projects to address flaws in their economic models, establishing absolute pricing power within the ecosystem.

2.1.1 Pendle

Pendle is currently the most successful in practicing this method. Both Penpie and Equilibria are auxiliary protocols enhancing PENDLE LP yields based on the Pendle veToken economic model, where LPs can receive Pendle mining boosts without staking Pendle. Their business models are not much different, and their main function is to absorb some of the selling pressure of the governance token, facilitating healthier growth for Pendle.

2.1.2 Lybra Finance

After V2 of Lybra did not achieve effective growth, it also began to deliberately create its own ecosystem projects. On October 13th, Lybra officially announced the start of Lybra War, positioning it as a focus for the next phase. Lybra's transparent launch of Lybra War is also because it recognizes many of its problems:

-

The high inflation of the governance token LBR due to maintaining high APRs, with V2 mining activities causing short-term excessive selling pressure.

-

Intense competition in the same track (such as Prisma, Gravita, Raft) leading to sluggish growth, with no investors behind Lybra to rely on.

-

Insufficient liquidity for eUSD, and the promotion and use of peUSD not meeting expectations.

-

Community consensus was shaken during the V1 to V2 migration, with doubts about the handling of "tokens not migrated in time" (the entire voting outcome was decided by sifu alone).

The core of Lybra War is the accumulation of dLP and achieving dynamic matching between dLP and eUSD. In Lybra V2, users must stake at least 2.5% of the eUSD value in LBR/ETH dLP to obtain esLBR emissions, so the second-layer protocols in Lybra's ecosystem must obtain more esLBR through yield boosting of esLBR and dLP. Additionally, the distribution authority in Lybra War is the esLBR emission among LSD pools, with potential demanders being LST asset issuers and large eUSD minters. The LSD pool depth mismatch in Lybra is more suitable for small LST issuers to accumulate esLBR to enhance their voting power in esLBR.

Currently, Match Finance is the core player involved in Lybra War, and an effective competitive landscape has not yet formed. Match Finance mainly addresses two issues (which are not elaborated here):

-

The problem of users not receiving esLBR incentives when minting eUSD without dLP;

-

The yield boosting of esLBR and the liquidity exit issue.

As protocol layers in the LSDFi track, neither Lybra nor Pendle are issuers of LST, hence their early accumulation of a large TVL through high APRs also planted a negative seed. For their future healthy development, they choose to develop ecosystem projects to continuously support themselves. In fact, any ambitious LSDFi leading project will inevitably embark on this path of development.

2.2 Micro-innovations to enhance differentiated user experience

For non-leading projects, identifying their unique positioning is key to maintaining their niche in a competitive sector. Even minor innovations can reach a specific user base, and if these users are highly engaged, the project has the means to survive.

2.2.1 No liquidation: Take CruiseFi as an example

While most projects are still competing over loan-to-value ratios and types of collateral, some have introduced a "no liquidation mechanism" to attract users.

For instance, CruiseFi allows users to stake stETH and mint the stablecoin USDx, which can then be exchanged for USDC through the USDC-USDx pool on Curve. Lenders providing USDC to the Curve stablecoin pool earn interest generated during the stETH staking period.

So, how is it ensured that borrowers are never liquidated? When a liquidation could occur:

-

The protocol locks a portion of the collateral (stETH) and allocates the staking yield of the locked stETH to the borrower;

-

Positions exceeding the stETH yield are suspended, ensuring that the staking yield always covers the borrowing interest, effectively preventing borrower liquidation. However, as the overall staking rate of ETH rises, the yield on stETH could decrease;

-

For suspended positions, Price Recovery Tokens (PRTs) are issued, which can be exchanged 1:1 for ETH (only when above the liquidation threshold) and can be traded on secondary markets.

The advantage is that borrowers can delay or avoid liquidation, lenders earn staking yields on ETH, and PRT holders can benefit from ETH's potential growth. "No liquidation" is particularly attractive to users with a higher risk appetite during bull markets.

2.2.2 Combined yield: Take Origin Ether as an example

In the DeFi world, yield is always the most attractive narrative, and this rule still applies to LSDFi.

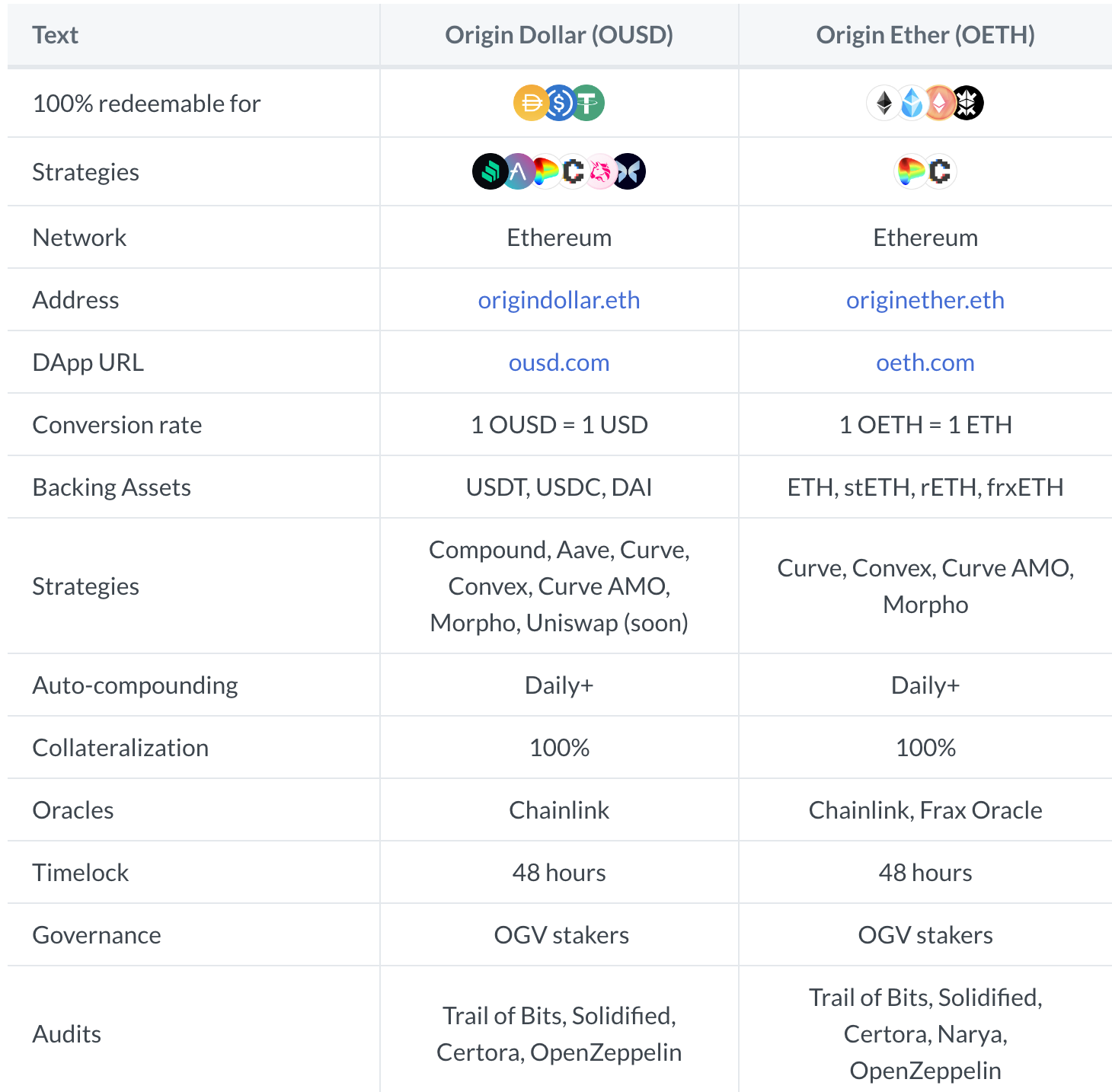

Origin Ether was launched in May 2023, using ETH and other LSTs as collateral, with the value of 1OETH always equal to 1ETH.

Origin Ether's main differentiator from other LSDFi is that its yield comes from a basket of LST assets like stETH, rETH, sfrxETH, etc. Additionally, OETH utilizes AMO strategies with OETH-ETH liquidity pools on Curve and Convex, and supports strategies on Balancer, Morpho, and other ETH-based Curve pools. Through optimized liquidity strategies, Origin Ether is able to offer users an APY above the market average, which is why it has rapidly accumulated a significant TVL in recent months (currently ranked seventh in market share).

2.2.3 Continuing to layer: Take LRTFi based on Eigenlayer as an example

LSDFi, as a nested structure within LSD, has reached a bottleneck, but the emergence of Eigenlayer could lead to another layer of LRTFi, presenting not just another leverage opportunity for the LSDFi sector but also a chance to recenter and expand into the market.

Although Eigenlayer is currently in a closed testing phase and not yet open to all users, the market excitement is evident from the two staking opportunities previously opened.

At the same time, several projects based on LRT (Liquid Restaking Token) have emerged, such as Astrid Finance, Inception, etc. The core logic of these projects is not innovative; they merely include LRT in the collateral range compared to LSDFi protocols. It's expected that this competition will intensify once Eigenlayer officially launches, with the sector still in its early stages.

2.3 Capital support, bundling with other mature projects, and enjoying bonuses from other ecosystems: Take Prisma as an example

For a newcomer to overtake competitors in a volatile sector without paradigm innovation, finding strong support and using the bonuses of other projects as an added buff can be an effective way to gain a foothold. This strategy could be termed "taking shortcuts" or "finding a godfather".

Prisma Finance is a prime example of such success. Unlike grassroots projects like Lybra Finance (community-driven, without private equity funding), Prisma is akin to a second-generation rich kid born with a silver spoon. Before any product launch, they managed to attract market attention with a glamorous press release. The most valuable information revealed was not about their project's distinct mechanisms, but rather about their investors list, which includes DeFi OGs like Curve and Convex as well as major institutions like OKX and The Block.

Prisma's development path followed its promotion, bundling with Curve and Convex and by securing their support, giving their native stablecoin mkUSD extra rewards (in the form of CRV and CVX) and leveraging the veToken model (which allows protocol parameter control) to create a flywheel effect.

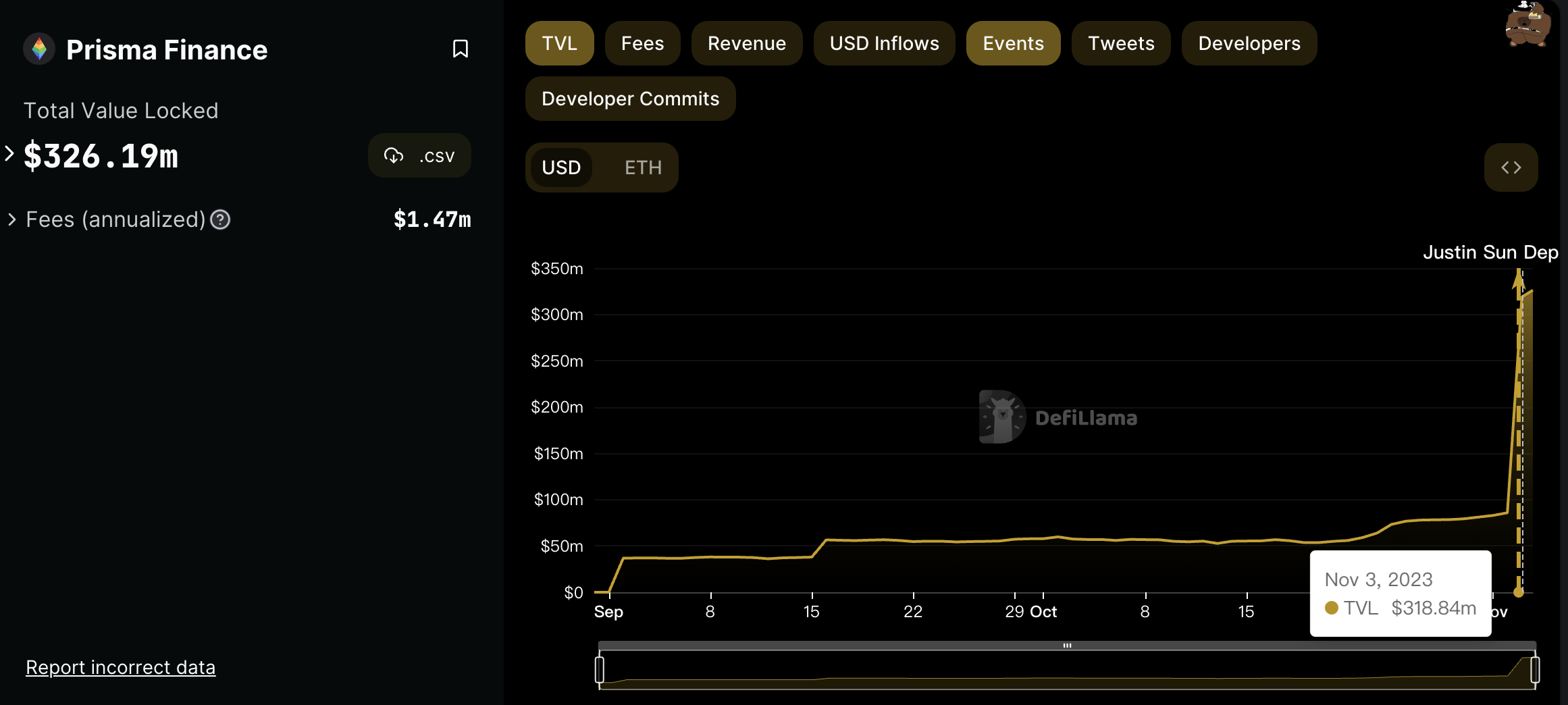

In its third month post-launch, supported by Justin Sun's $100 million worth of wstETH, Prisma's TVL hit an all-time high, surpassing Lybra to become the new leader of the track.

2.4 True paradigm innovation

Whether on an industry-wide scale or within a specific sector, after rapid growth, there often comes a bottleneck in development. The fundamental solution to such predicaments is undoubtedly "paradigm innovation".

Although LSDFi hasn't yet seen innovation capable of changing the game, I firmly believe that as long as the value of Ethereum continues to be a strong consensus, there will eventually be a paradigm-shifting innovation that reignites the fervor in LSDFi.