This article was translated by Notion AI and originally written in Chinese, published on the Blocktrend website.

If you have ever held USDC or BUSD stablecoins, or used Coinbase or FTX exchanges, then you have indirectly been a customer of Silvergate, a US bank.

Many exchanges claim to be bridges connecting cryptocurrency and fiat currency, but the real hero behind the scenes is the “crypto-friendly bank” that is willing to manage deposits in currencies such as the New Taiwan Dollar and the US dollar for exchanges. In Taiwan, there are banks such as KGI Bank and Far Eastern Bank, while in the United States, they are Silvergate Bank and Signature Bank.

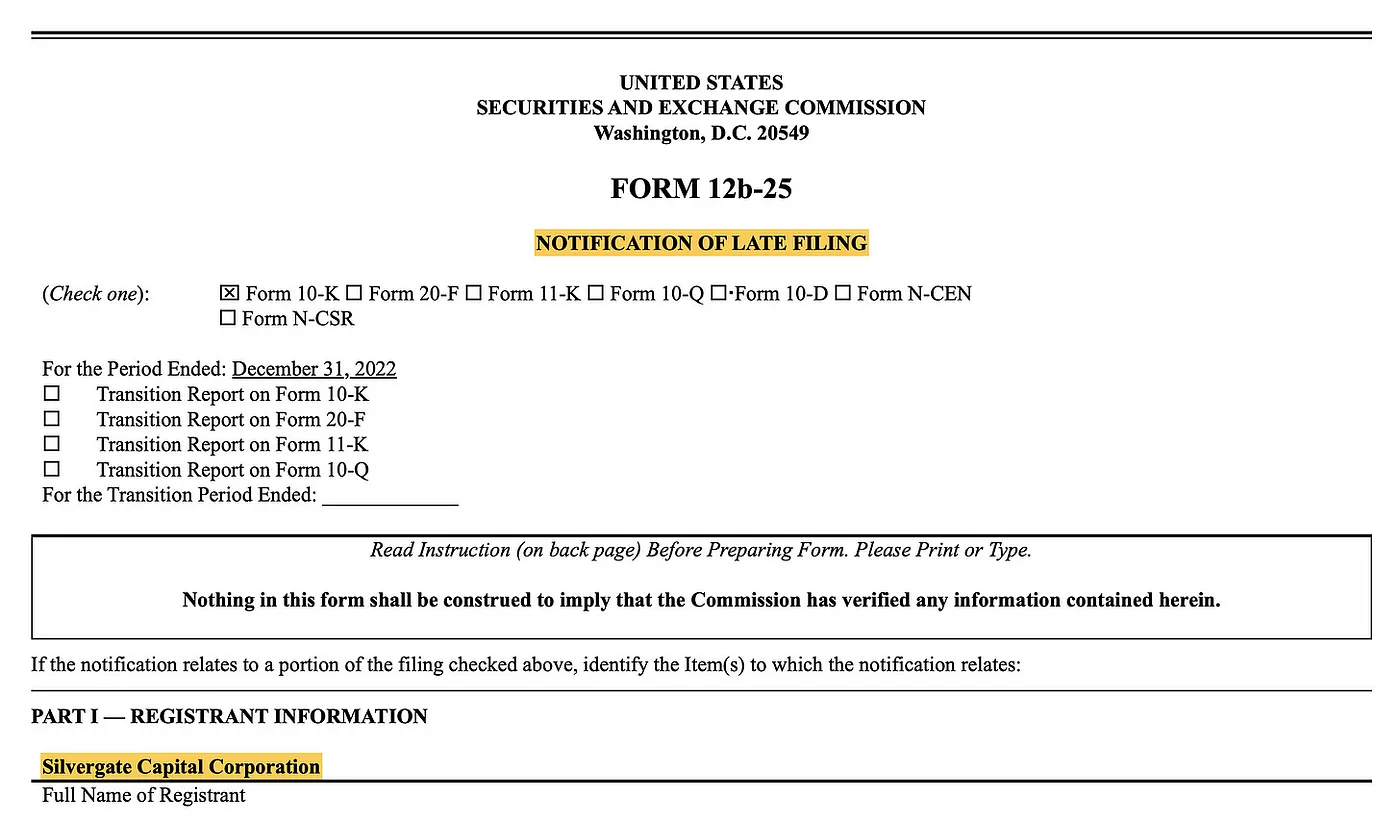

Since 2013, Silvergate Bank has been a reliable partner of exchanges. However, this small bank that has been deeply involved in the cryptocurrency industry for 10 years is currently facing its largest operational crisis since its establishment in 35 years, due to market factors. Silvergate Bank lost over 8 billion US dollars in deposits last quarter, and last week, it not only saw its stock price plummet by 60% in a single day due to its failure to submit financial reports to the US government on time, but also forced its former allies to cut ties.

Those who have experienced the FTX incident personally know that they need to be careful about the domino effect. This article will first explain how Silvergate has developed from a small bank with only three branches to a financial center in the cryptocurrency industry, and then discuss the reasons behind its current operational crisis and the impact of a bank run on the market.

Network effects

The easiest way to enter the cryptocurrency industry is to buy cryptocurrency. By registering an account with an exchange, linking a bank account, and transferring New Taiwan Dollars to the exchange’s designated bank account, the New Taiwan Dollar balance will appear in the individual’s exchange account in just a few seconds. Then, you can use New Taiwan Dollars to buy cryptocurrency.

The process seems simple, but there are many difficulties behind it. Most banks do not do business in the cryptocurrency industry because of unknown risks or small scale, and exchanges face obstacles in opening bank accounts that can manage New Taiwan Dollars. The same dilemma also occurs in the United States. Silvergate Bank is a regional bank established in 1988, and unless you are a resident of California, you may never have dealt with Silvergate.

The turning point came in 2013, when Silvergate CEO Alan Lane first encountered Bitcoin. Unlike most bankers who only saw the risks, Alan Lane also saw the financial revolution behind Bitcoin, which theoretically allows people to manage digital assets on their own and become their own banks without relying on third-party custody. Although he may have only had a rudimentary understanding of Bitcoin at the time, Alan Lane did the same thing that most people entering the cryptocurrency industry do: he bought some cryptocurrency.

Alan Lane found that exchanges were always shut out by banks during the process of buying cryptocurrency. As a bank CEO, he decided to make a bold attempt to provide banking services to exchanges. In an interview with CNBC, he said:

I wanted to connect these two industries. Although this could disrupt the rules of the banking industry in the long run, in the short term, these companies need banks. They have not done anything wrong, illegal, or unethical. If they do something wrong, we will refuse to provide services.

Even in 2023, there are still very few banks willing to do business in the cryptocurrency industry. Therefore, ten years ago, just hearing that Silvergate was willing to do business with exchanges, many companies rushed to deposit US dollars, not seeking interest on deposits, but satisfied as long as they could send and receive US dollars through the bank.

For banks, these are zero-cost funds. Is there anything more enjoyable than this? Silvergate’s listing prospectus proudly states that its biggest advantage is being able to obtain a large amount of interest-free deposits from cryptocurrency clients. Silvergate’s business strategy is not to pursue higher borrowing rates, but to focus on serving these users and attracting more interest-free deposits.

After starting to do business in the cryptocurrency industry, Silvergate also found that the traditional financial system could not meet the needs of cryptocurrency clients. Cryptocurrency operates 24/7, but the financial system of banks has working hours. Therefore, Silvergate launched its own bank internal transfer service, the Silvergate Exchange Network (SEN). Its function is simple but practical: it allows USD transfers between Silvergate users 24/7, just like cryptocurrency.

This created a network effect. There is a frequent need for fund transfers between exchanges, and if everyone is a Silvergate customer, they can use SEN internal transfers to improve the efficiency of fund transfers. Otherwise, it takes longer for wire transfers or ACH transfers to arrive. Therefore, Silvergate’s customers will actively help attract business and inquire about potential partners: “Are you a Silvergate customer? Are you on the SEN network?”

With the courage to do business in the cryptocurrency industry and provide the SEN internal transfer service, Silvergate’s revenue has been soaring, and it was listed on the New York Stock Exchange in 2018. With the bull market in the cryptocurrency industry, Silvergate’s stock price even hit a historic high of $239 in November 2021. The “Stock Goddess” Cathie Wood and Wall Street market maker Citadel have both held a large amount of Silvergate stock. Silvergate has become a concept stock for the cryptocurrency industry in the banking industry.

However, now Silvergate’s stock price has plummeted over 97% from its high point, with only about $5 per share remaining. The key lies in the FTX exchange’s bankruptcy in 2022, which caused market panic, and Silvergate’s own risk control problems.

Bear market and Black Swan events

In 2022, the cryptocurrency industry entered a bear market, and Silvergate’s stock price was inevitably affected. However, Silvergate is fundamentally still a bank and has experienced bull and bear market transitions before, so it should be able to weather this storm. Even Silvergate previously stated that the advantage of operating in the enterprise market is that it is relatively stable, and institutional investors are not as “fickle” as retail investors.

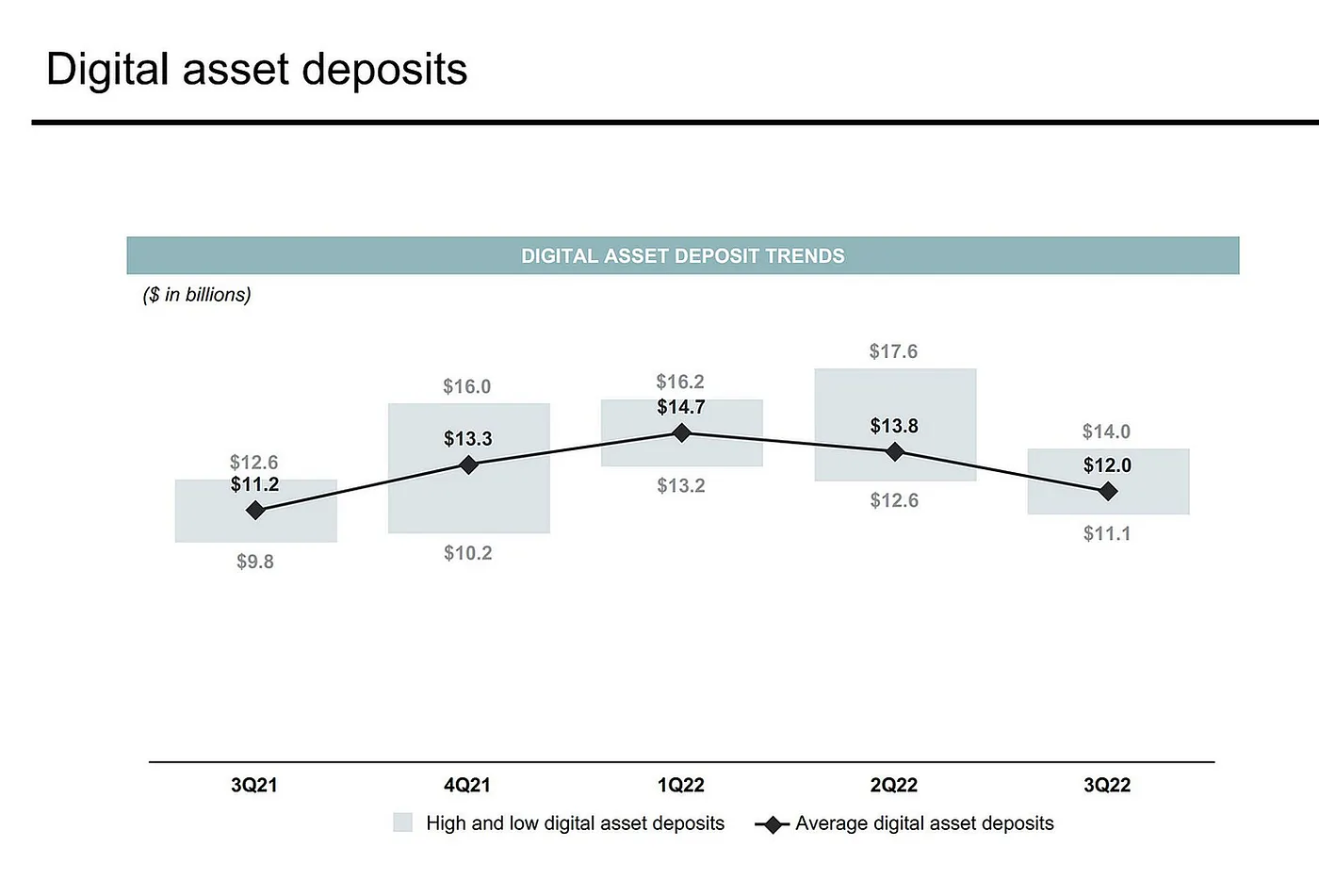

This is also reflected in the numbers. The following chart shows the total deposits held by Silvergate for cryptocurrency clients before the third quarter of 2022. Although the total deposits decreased from a high of $14.7 billion to $12 billion in 2022, it can be said to be quite stable compared to the drop in cryptocurrency prices, and the total deposits are still higher than they were one year ago.

However, no one expected the FTX bankruptcy and Silvergate’s own risk control issues to cause them to lose all the profits they had made in the past few years in the second half of 2022, and even jeopardize the bank’s survival.

FTX is one of Silvergate’s important customers. The bankruptcy of FTX at the end of last year made many investors lose confidence, not only selling the cryptocurrency in their hands, but even determined to withdraw from the cryptocurrency industry. At that time, the market atmosphere was quite panic-stricken, and various exchanges were processing a large number of user withdrawals. If an exchange acted too slowly, people would worry if it would become the next “FTX”.

As the “fiat currency vault” of exchanges, Silvergate has to bear even greater pressure. Even last year, they had to deal with a significant amount of withdrawals from FTX users. This made Silvergate’s deposit balance drop significantly, and many people began to worry about the bank’s risks. Although Silvergate issued a statement at the time, saying that the bank’s balance sheet was still strong and there was no need for customers to worry, it did not dispel the panic in the market.

As an exchange, Silvergate’s “fiat vault” is under greater pressure, with bank deposits flowing out as high as $8.1 billion in the fourth quarter of last year alone. People thought the most difficult time of panic had passed, but they overlooked the fact that Silvergate had already suffered severe damage from coping with a large number of withdrawals in a short period of time. Banks are most afraid of runs, and the changes in the global economic environment have hit Silvergate harder.

Starting in 2020, the US Federal Reserve and other central banks around the world have successively announced interest rate cuts, forcing money into the market to stimulate consumption and drive the economy. This was also the beginning of the previous round of the cryptocurrency bull market, with various exchanges bringing in large amounts of cash to Silvergate. Although the money was zero-cost, the bank still had to find a way to generate income. Silvergate eventually chose to invest in US bonds, which is quite consistent with its pursuit of stability.

However, at that time, the investment return rate for short-term US bonds was extremely low. For example, the annual yield on three-month short-term US bonds was only 0.01%, almost like putting money under a mattress. Therefore, Silvergate mainly invested in long-term US bonds of 5 to 10 years or more, generating an annual return rate of about 1% to 2%. These funds accounted for 70% of Silvergate’s total deposits.

People familiar with risk management will surely frown upon seeing this: “Silvergate is investing the exchange’s money in long-term US bonds?”

The longer the maturity of US bonds, the lower their market liquidity. In other words, if Silvergate needs to sell these long-term US bonds for cash, it will inevitably have to sell them at a discount. This means that Silvergate was gambling that there would be no major crisis in the cryptocurrency industry in the next few years, which was clearly too optimistic.

As we all know now, the US Federal Reserve began to raise interest rates, causing the value of previously purchased bonds to decline, and then FTX’s collapse triggered a panic run. To cope with the withdrawal demand, Silvergate was forced to sell long-term bonds at a loss. The more they sold, the more they lost. In the fourth quarter of last year, Silvergate sold $5.2 billion worth of bonds and lost $750 million due to early sales, which is equivalent to a 15% discount.

The key point is that the vast majority of these are not Silvergate’s own funds, but assets temporarily deposited by cryptocurrency users. In the event of another run, Silvergate will face even greater losses and may eventually become insolvent. Even if Silvergate has already drastically cut staff and reduced operating costs, it is still not enough to cope with the situation.

The Unknown Bomb

Last week, Silvergate sent a letter to the US Securities and Exchange Commission notifying them that their financial report would be delayed, pushing the company into an abyss.

“Can the money inside be safe if they can’t even submit their financial report on time?”

Not only did Silvergate’s stock price plummet by 60% in a single day, but cryptocurrency companies also couldn’t sit still and jumped out to cut ties, saying they had transferred their assets to other banks. Everyone is worried that if the cryptocurrency financial center Silvergate catches fire, it will have a wide impact. Just like FTX’s collapse didn’t just hurt FTX users, the fire spread and even the cryptocurrency media CoinDesk and its parent company Digital Currency Group (DCG), who originally exposed the scandal, suffered losses.

If the stablecoin issuer puts their US dollar reserves in Silvergate but can’t get them back, causing the stablecoin to decouple from the dollar, there may be an even bigger tsunami. Fortunately, major stablecoin issuers such as Tether, Circle, and Paxos have all released statements clarifying that they no longer keep their money in Silvergate. Major exchanges such as Coinbase, Kraken, and Gemini say they have already transferred their funds to other banks, such as Signature.

Although there is no immediate danger at the moment, after a few days of customer runs, Silvergate is likely to lose even more than before. In addition to shareholders losing money, it is unknown whether users will also lose money. However, the reason why the market is not as panicked as it was when FTX collapsed may be because Silvergate is ultimately a member of the US banking system, and user assets are also protected by the Federal Deposit Insurance Corporation (FDIC), theoretically avoiding a tragedy like FTX’s collapse without anyone to help.

In terms of industry development, there are not many banks willing to take on cryptocurrency-related businesses. Silvergate’s poor management has caused the cryptocurrency industry to lose an important and influential ally. Although US regulators have not yet used Silvergate as a reason to restrict banks from providing financial services to the cryptocurrency industry, and have allowed banks to assess risks on their own, if politicians want to use risks as a topic, Silvergate’s incident may be the material they need.

In the final analysis, although Silvergate’s incident was caused by market turmoil in the cryptocurrency industry, the problem is not with cryptocurrency itself, but with the bank’s risk management. Silvergate is a publicly traded company and is subject to strict supervision. It made such an obvious mistake, and the government is only reacting after the fact. On the other hand, the 24/7 transparent on-chain financial market can rely on the eyes of the people to uncover potential problems might be better.