Note: Originally posted Nov 17, 2021 on Substack.

In the current market, bitcoin is without doubt a short-volatility risk-on asset that benefits from the ongoing financial environment driven by perpetual government debt expansion. However, bitcoin’s position as a borderless asset with immutable monetary policy poses the question as to whether it has the potential to become a global long-volatility asset that could serve as a safe-haven should serious issues develop in the current financial system.

The biggest proponent of this theory is Greg Foss, a former credit trader who’s bitcoin investment thesis is built around modelling the cryptocurrency intrinsic value as a credit-default-swap insuring against sovereign debt defaults.

The goal of this writing is to discuss what characteristics one should expect if bitcoin has the potential to act as this insurance policy, and to look at, as Foss would say, the recent gurgling of the financial system to examine how well the thesis is holding up or showing cracks.

If Foss’s thesis is accurate, I believe we should expect:

- Bitcoin is usually a risk-on asset, therefore without imminent financial distress it should be negatively correlated to the CBOE Volatility Index (VIX).

- In times of small panic (ie: stretched equity valuations) bitcoin should maintain its negative correlation to the VIX—or become increasingly negative as traders reduce their risk exposure.

- In times of true global panic, bitcoin should transform into a risk-off asset and its correlation to the VIX should increase.

- If the panic surrounds debt defaults, we should expect a falling correlation to High Yield Debt (and possibly Treasury Bonds), with a rise in correlation to gold and other hard assets.

- We should also expect bitcoin’s correlation to sovereign CDS rates to increase (this will not be examined in this writing, but sovereign CDS should correlate highly with High Yield Debt + Treasury Bonds).

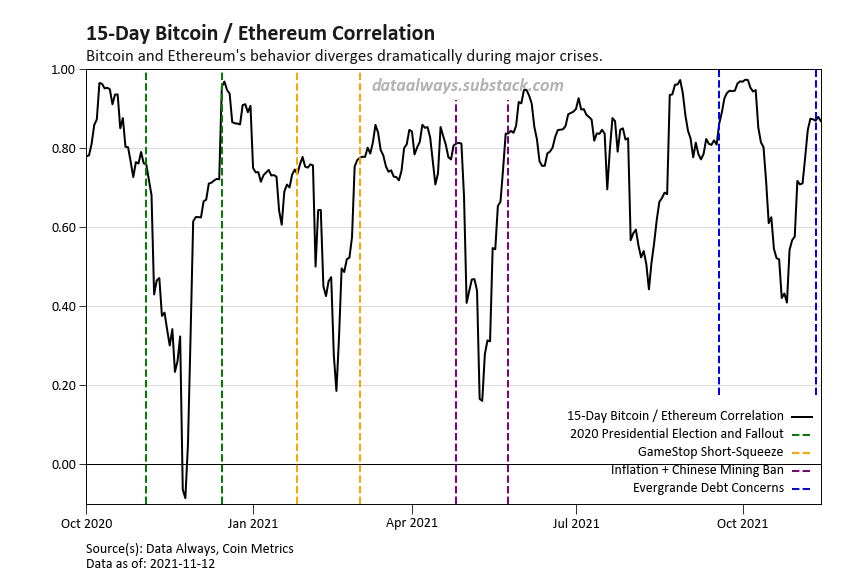

- In times of global panic, bitcoin should outperform other major cryptocurrencies and the correlation between bitcoin and ethereum should fall.

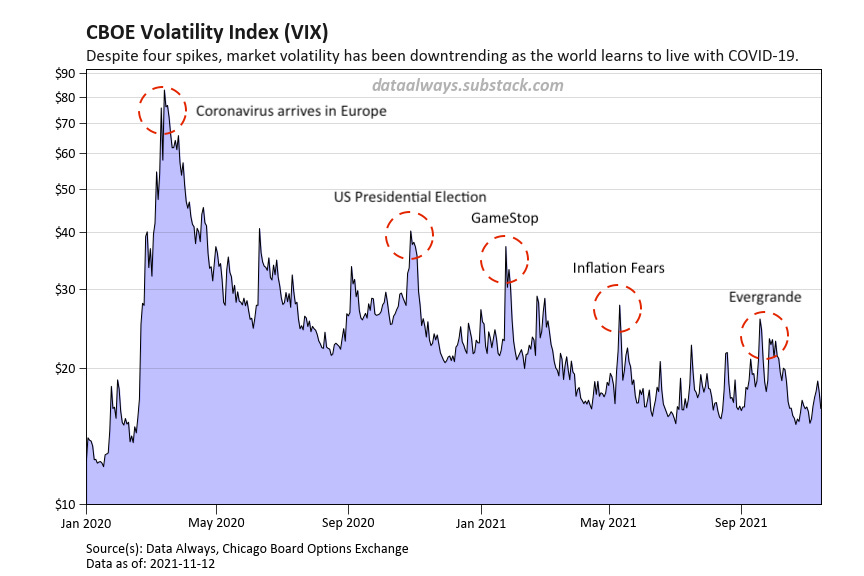

For the sake of this analysis, the focus is on modern bitcoin: post-pandemic with moderate and increasing institutional adoption. There have been four large volatility spikes of interest since the liquidity crisis at the outbreak of the pandemic: the US presidential election, the rise of GameStop, the first clear tick-up in inflation, and the beginning of the collapse of the Chinese real-estate market when it became a clear possibility that Evergrande could default on its debt.

The VIX spike in May 2021 surrounding inflation fears was simultaneously timed with the increased crackdown on cryptocurrency mining in China—compromising the data and making it not worth investigating.

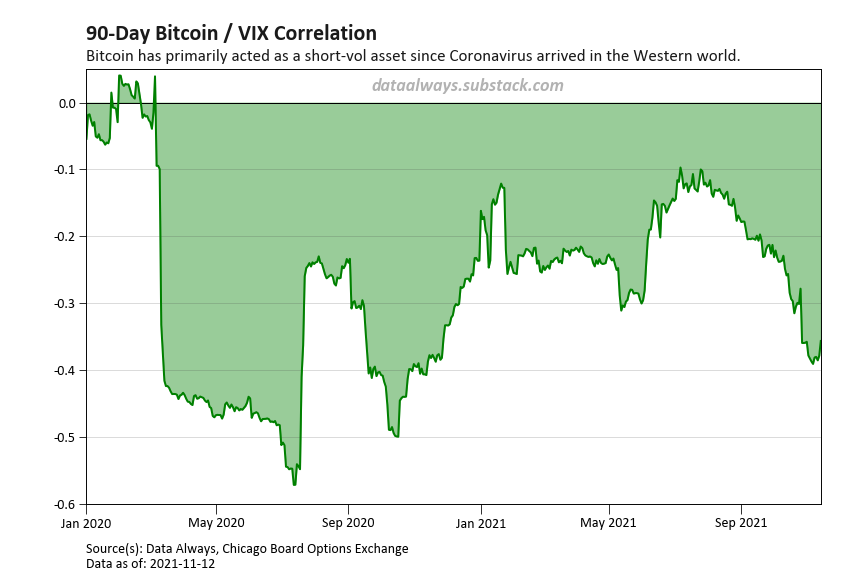

Seen in the figure below, leading into the pandemic, the correlation between bitcoin and the VIX was extremely low. As the liquidity crisis began the long-term correlation dropped into deep negative territory and has stayed there since. Despite some short-term volatility in the correlation, bitcoin has remained a risk-off asset that is benefitting from low interest rates and massive global stimulus.

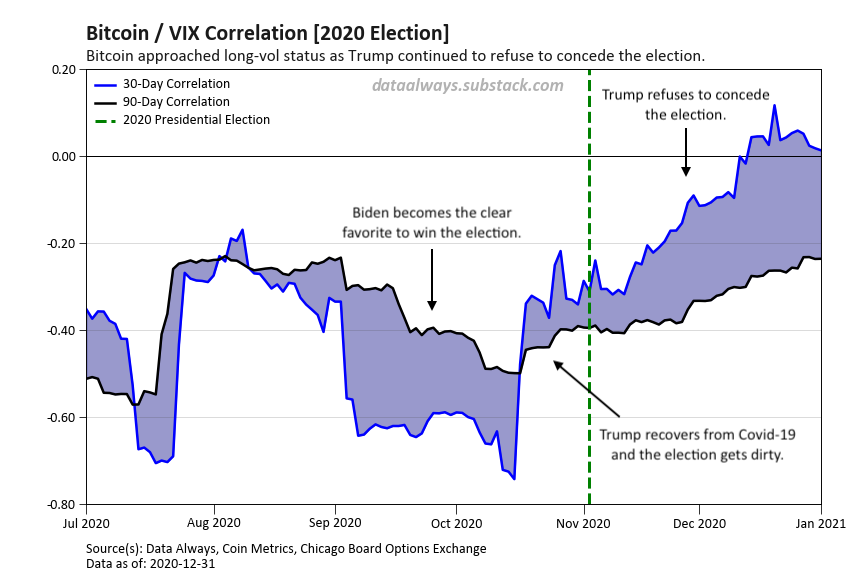

Turning to the volatility spikes, around the 2020 US Presidential Election, comparing the 30-Day to the 90-Day Bitcoin vs. VIX correlations there were three very distinct phases:

- In September 2020 it became overwhelmingly likely that Joe Biden was going to beat Donald Trump in the November election. This is reflected in FiveThirtyEight’s election forecast as it transitioned from a 67% chance of victory on August 31st to a 86% chance on October 12th when Trump was cleared of Covid-19 (contracted October 2nd).

- The Bitcoin / VIX correlation became increasingly negative during this period as the financial world began to believe that a Biden presidency would work quickly to restore global stability. This indicates that bitcoin briefly reaffirmed itself as a short-volatility risk-on asset.

- Once Donald Trump was cleared of Covid-19 the election became increasingly nasty with the release of files allegedly from Hunter Biden’s laptop, Trump raising doubts about whether he would concede the election, and the Supreme Court getting involved with Pennsylvania’s mail-in ballot deadline extension.

- At this point, the financial world started to get uneasy and we saw the VIX begin to increase. Simultaneously we saw the short-term (30-Day) Bitcoin/VIX correlation jump above the long-term (90-Day) correlation. For the thesis in this writing, it appears as if instability in the US political system began to make Bitcoin look like a better (relatively,) risk-off asset.

- On November 4th, 2020 Joe Biden won the US Presidential election—and Donald Trump refused to concede before the end of the year.

- During this period, the short-term correlation continued to rise and outpace the long-term correlation. Bitcoin briefly became uncorrelated to the volatility in the traditional markets and showed signs that would be expected from a risk-off asset.

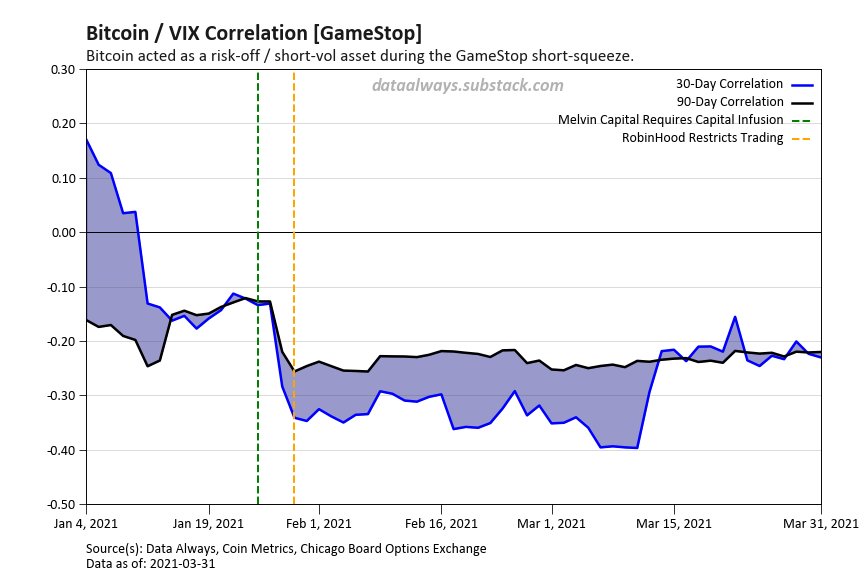

Contrasting the US Presidential Election, GameStop’s rise was the epitome of a financial risk-off event that never risked any true global instability. This presents itself very clearly in the figure below: the correlation between Bitcoin and the VIX dropped sharply as the financial world was caught off guard, but no one rushed into bitcoin to protect their assets when meme-stocks went to the moon.

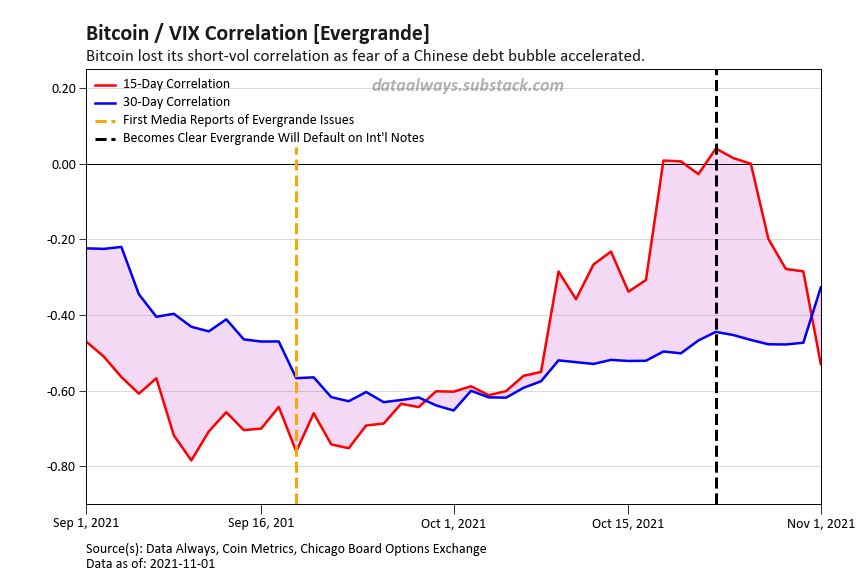

Moving on to the Evergrande debt defaults, switching to 15-Day and 30-Day correlations, the bottom for the 15-Day correlations coincides with the first media reports that Evergrande was in serious financial distress. As the story continued to play out and it became clear that Evergrande was not going to be able to pay the interest on all their debt, the 15-Day correlations continued to rise until Bitcoin briefly became uncorrelated with the CBOE Volatility Index. As the situation calmed down and panic receded, the 15-Day correlation once again fell back to long-term negative levels.

In the three situations examined above, bitcoin’s correlation to the VIX behaved exactly as the thesis predicted, but how did it behave relative to ether, the world’s second largest—and more traditionally risky—cryptocurrency?

In the figure below there is a clear pattern of falling short-term correlations between the two major cryptocurrencies around these financial market volatility spikes. The timing seems to lag slight and more data should be examined, but there are definitely signs that suggest it could be a good indicator.

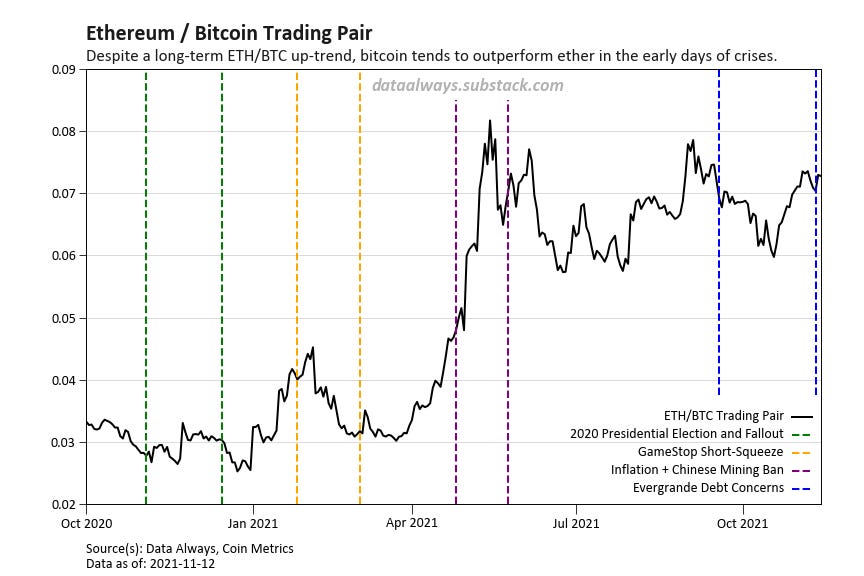

If the thesis is correct, it is also expected that during these times of panic in the financial system that bitcoin should outperform ether—being the risk-off asset of the cryptocurrency space. The chart below seems to confirm that—of course more data would ideal, but even with a general up-trending ETH/BTC trading pair, following these volatility spikes, the trend is for bitcoin to outperform ether.

It’s important to note that during the periods of time examined above, bitcoin has not performed exceptionally well—the correlation, although rising, has generally been negative during the crises that were examined. But the early signs are there, and although some of the crises pushed the financial world to the edge of its comfort level, none of them evolved into cataclysmic events that spawned large contagion into the rest of the market.

I think Foss might be on to something, but it’s a tough thesis to take on faith. A risk-on asset that could transform into a risk-off asset if the financial world collapses… sounds almost too good to be true.

-T.