Today’s piece is a look at some less-common Ethereum (and ETH/BTC) charts that explore some of the unexpected behavior from this bear market and provide insight into what we might expect going forward.

Bear Market Drawdowns

One of the big stories of this bear market has been the relative performance of Ethereum and Bitcoin. In the 2018-2020 bear market, Bitcoin severely outperformed Ethereum and gained the moniker of crypto reserve asset, as the pristine non-stablecoin choice to hold as the market sells off. We’ve seen glimpses of truth to the name in 2022, but currently Ethereum is down less from its all-time high than Bitcoin, despite running up far more aggressively in 2020-2021.

If Bitcoin isn’t going to outperform Ethereum in a bear market, one of the main selling points in terms of portfolio diversification choosing to include Bitcoin is greatly diminished.

Divergence from the TradFi metaphor to ETH/BTC

With Bitcoin favored by most macro and energy investors, the bitcoin vs. ether dynamic has often mirrored the dynamic between tech stocks and industrials. In the figure below we see that the ETH/BTC trading pair as often acted as a levered QQQ/DJI pair, yet at times the correlation breaks.

As tech stocks have retraced most of their excess gains from July following Powell’s comments at Jackson Hole on August 26th, the correlation has again broken down, suggesting that although tech stocks have displayed weakness compared their industrial counterparts, Ethereum has held up well compared to Bitcoin. Is this another tailwind leading into The Merge or is there further downside to come in the ETH/BTC pair?

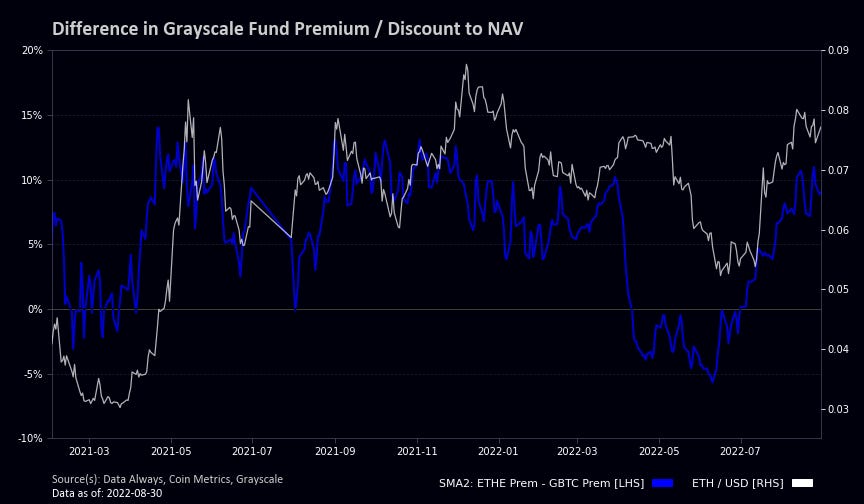

Grayscale discounts as a momentum indicator

Taking a quick view of the institutional landscape, we see in the figure below that the divergence in premiums/discounts attached to Grayscale’s Bitcoin and Ethereum investment trusts has acted as a leading indicator for the performance for the ETH/BTC pair.

Since the start of July, GBTC has once again begun to trade at a steeper discount than ETHE, quickly followed by the ETH/BTC trading pair climbing back near cycle highs. The divergence in discounts does seem to be stabilizing in the region it has historically settled, which could suggest that extreme short-term out-performance is less likely, but unless we see ETHE sell off compared to its net asset value, I suspect that the current relative dynamics would be bullish for the ETH/BTC pair.

Realized volatility

Looking at the relative realized volatilities for ether and bitcoin, ether’s volatility is accelerating in comparison and beginning to approach levels seen in large macro events like the outbreak of the COVID-19 pandemic and the Chinese mining ban. The relative volatility level remains significantly below what we saw during DeFi Summer in 2020, which although a major event is dwarfed in significance by The Merge, thus I would expect ether’s excess volatility to continue climbing over the next couple months. Volatility is generally perceived as bad, but volatility can be both to the upside or to the downside.

A breakdown in altcoin correlations

One metric that I’ve historically found very interesting is the difference in altcoin correlations to bitcoin and to ether. During bull markets and times of market calm, we tend to see altcoin correlations to ether outpace their bitcoin correlations, but as liquidity starts to dry up in the market and correlations either collapse or all go to one, we see a narrowing of the difference—times where bitcoin/altcoin correlations have been larger than ethereum/altcoin correlations have traditionally been signs that taking a risk-off stance is appropriate.

Right now, we’re again seeing a very slightly inverted correlation, and although a dangerous proposition it’s an interesting proposition that this time might indeed be different. With The Merge being a positive ether-only exogenous factor, it is reasonable to expect that we would see a breakdown in the accuracy of this metric.

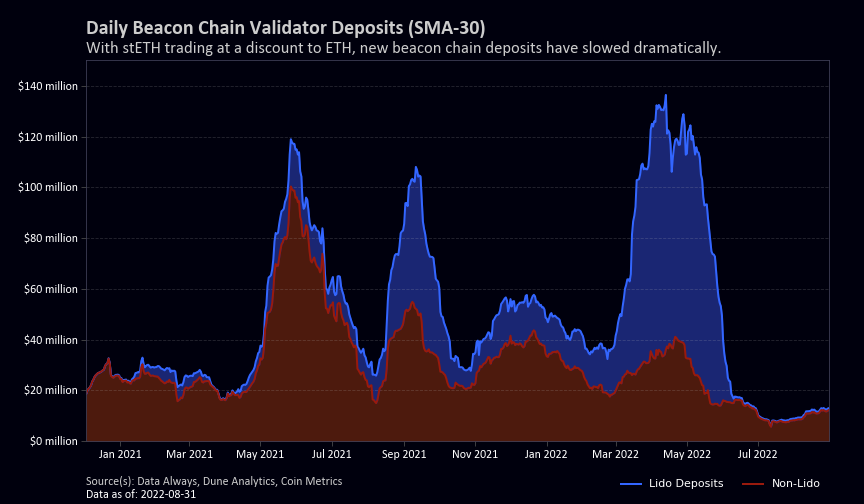

Daily beacon chain deposits

On the topic of the beacon chain, the story for March and April 2022 was the growth of Lido and stETH, but the story the past four months has been stETH’s trading pair discount, which has halted essentially all new validator inflows into Lido.

This is a double-edged sword. On one hand it’s great for validator decentralization as Lido’s share growth stopped before it gained the ability to attempt to stop block finalization, but from a ETH/USD perspective it has removed a lot of spot demand as funds like Celsius are no longer levering up to chase yields.

Healthy long-term, but one of many causes for the poor price performance since mid-May.

Validator deposits in profit

It is unclear whether histograms of validator deposit prices are a useful tool for gauging potential sell pressure once withdrawals are enabled. However, by looking at the evolution of the profile we can break depositors into regions: early depositors who are unlikely to sell and are well in profit, Lido depositors who have been able to exit at any point, and late-coming retail who make up a significant aspect of underwater depositors, but also who are overrepresented when not separating out Lido’s share.

All things considered, if the price remains at these levels until withdrawals are enabled, I suspect that the number of validators choosing to exit would be far lower than many estimates.

Realized Capitalization Impulse Signal

An experimental metric that I’ve been playing around with is trends in realized capitalization impulses. A more detailed examination will follow, but Ethereum is now in a zone that historically has suggested risk-neutral to be a smart choice.

As far as how I’ve been modifying my positioning: I trimmed my size in early-mid August as the market began to look toppy, and am still waiting for a bullish driver to begin re-opening positions. Whether this is a change in market conditions or a successful Merge, until that happens I think the risk/reward just isn’t great as ether continues to be tossed around by macro conditions.

All things considered, we have a lot of competing bullish and bearish narratives. This is normal around binary events and makes positioning extremely difficult. Until The Merge (only two weeks!) it’s likely we won’t get any particularly meaningful crypto signals, but it’s important to not find yourself improperly positioned for the CPI release on September 13 or for the FOMC meeting later in September.

Tough market to trade, no surprises there.