Introduction

Celsius is a custodial wallet which provides users a way to earn yield on their crypto. The company behind the wallet was formed in 2017 during the ICO boom where they raised approximately $50 million USD. Since launching in 2017 Celsius has grown to have ~$17 billion USD in assets under management (AUM), 1.5 million registered users, 500k active users, thousands of corporate accounts and has paid a billion dollars in yield to their community. Celsius has also launched CelsiusX which is a strategic DeFi play by the company.

Celsius positions itself as being a community of holders, not traders. Alex, the CEO and Co-Founder, frequently market Celsius as a way of “keeping more of your coins” - they offer fee free withdrawals/loans/swaps, provide yield, and limit active trading on their platform.

It’s important to remember that almost all aspects of Celsius occur through mechanisms of centralization which are antithetical to much of the crypto ecosystem and philosophy. Many of the products offered by Celsius also exist in purely decentralized form as well. There are tradeoffs to both approaches. Each product in the Celsius ecosystem comes with the standard risks of centralization: single points of failure which can be exposed by hackers, coercion by governments, fundamental lack of transparency, harder to detect corruption and bans without appeals. However, the centralization of Celsius provides many positives such as lower fees, human support systems, infrastructure management, simpler to use abstractions and bridges into the existing financial system. Every user has to decide for themselves whether the risks of centralization outweigh the benefits.

Founders

Celsius has three co-founders: Alex Mashinsky, Daniel Leon and Nuke Goldenstein. Alex is the face of Celsius. He is a serial entrepreneur and has made 3 unicorns with over $3 billion in exits, much of which came before the financial crisis of 2008 which caused asset inflation. Alex was a critical innovator of VOIP and has several patents on it. Many accuse Celsius of being a scam by the founders, it’s up to each potential user/investor to determine the liklihood of that being true considering the professional history of the founding team members and the way they run this business. I personally do not believe Celsius is a scam considering the social and business prominence of Alex and the values he instills into his community and company.

Consumer Products

Earn

The first product Celsius created was their Earn product which allows users to earn yield on the assets they’ve deposited in the Celsius platform. Celsius provides users this yield by loaning user assets to, for example, hedge funds at 10% and then paying the user 8% while pocketing the difference. Celsius claims that up to 80% of the yield they generate goes back to the user. Celsius also generates yield by putting user assets into DeFi platforms like Uniswap where the company earns yield for providing liquidity.

Celsius offers user the ability to earn yield in kind or earn in CEL, the native token of the Celsius platform. Earning in kind means earning interest in the same asset as what’s deposited (for example earning BTC interest on BTC deposits and ETH interest on ETH deposits) while earning in CEL means earning interest in the CEL token (for example earning CEL on BTC or CEL on ETH). Users who earn in CEL get a yield boost. For example, users get 6.20% earning BTC on BTC while they get 7.81% earning CEL on BTC.

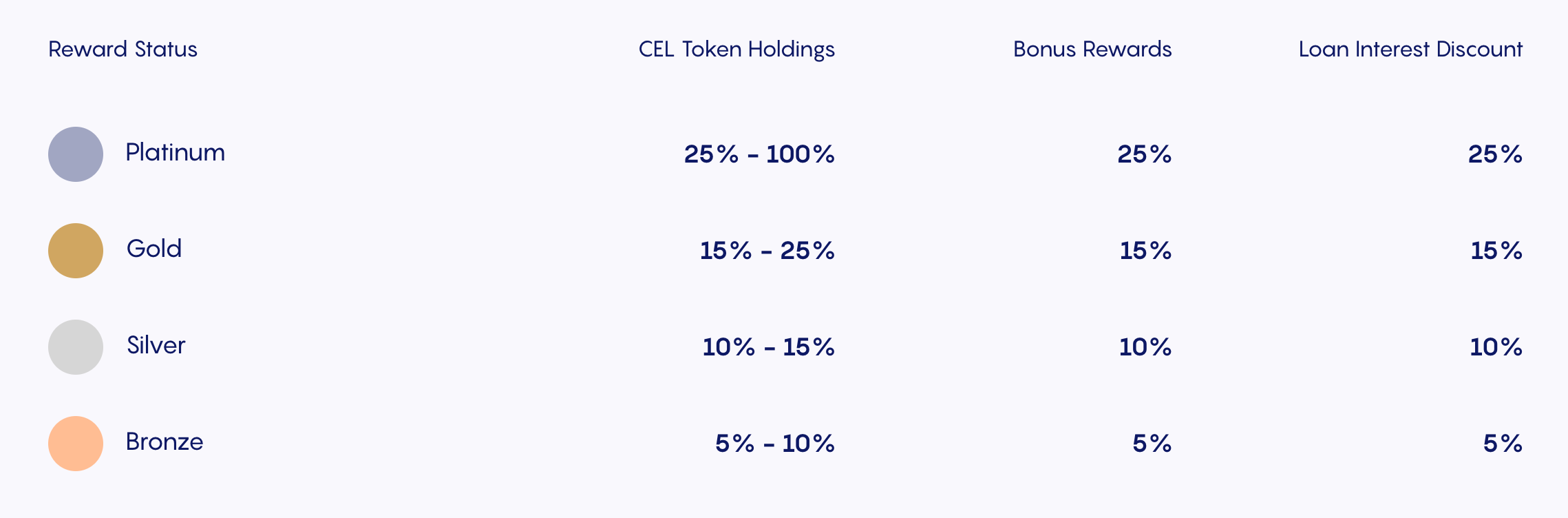

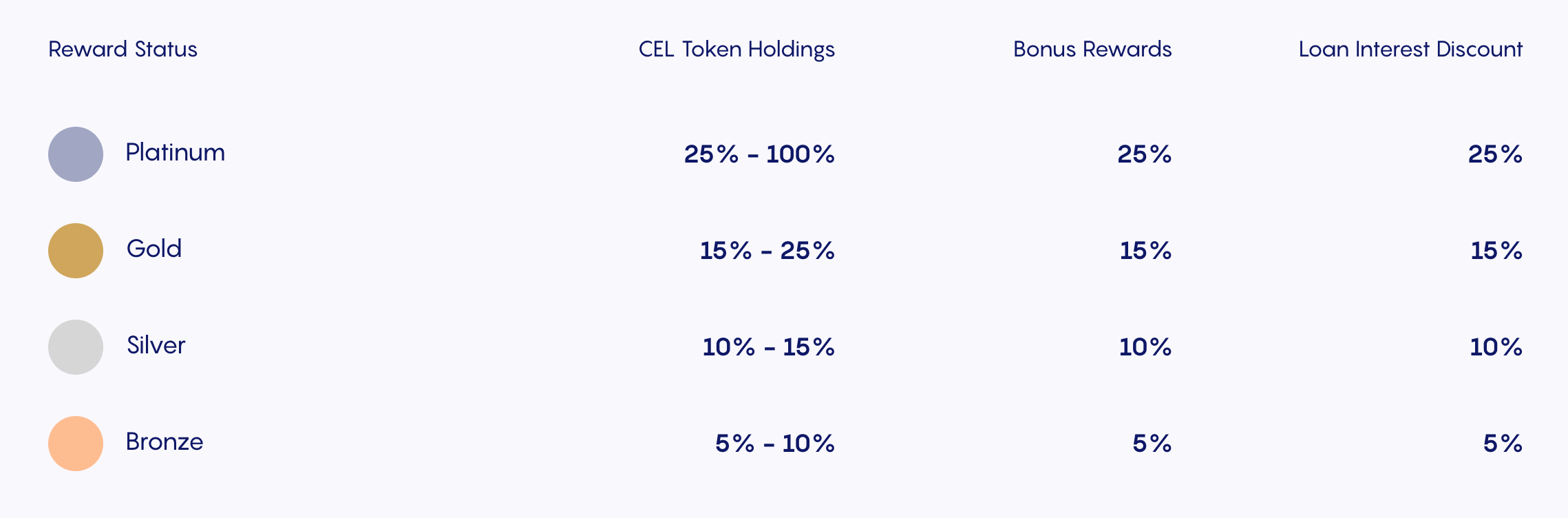

Celsius has a bonus rewards based on how much CEL a user has in their wallet.

The reward tiers are based on the percentage of a users portfolio held as CEL but measured in USD. If a user has $100 of non-CEL assets and $5 of CEL (for a total portfolio value of $105) then they will be in the Bronze tier and will earn an extra 5% on their rewards when earning in CEL.

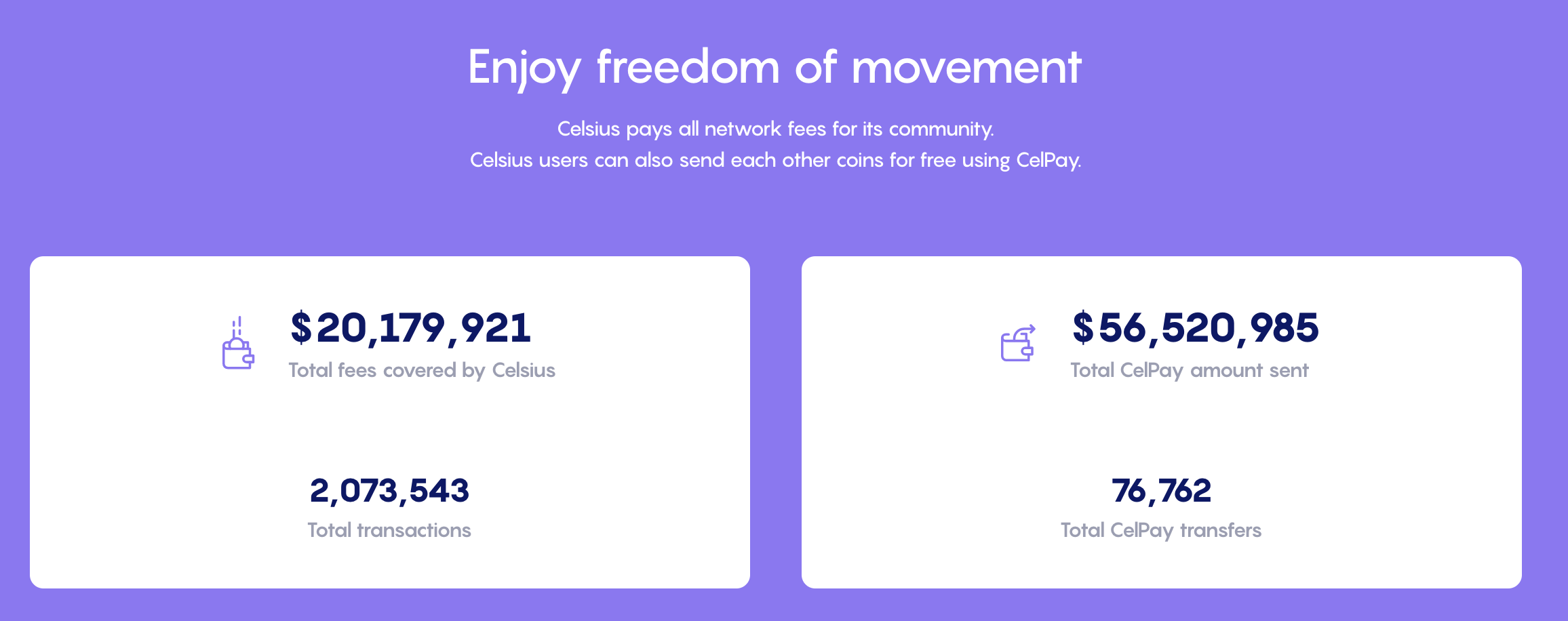

Celsius offers 0 fee withdrawals from their wallet as well. Since inception the company has covered over $20 million in network fees.

When a user elects to earn their yield in CEL they put buying pressure on the coin because Celsius pays CEL yield through open market purchases. Every week the company goes to various exchanges to purchase CEL which needs to be paid to users earning yield in CEL. In addition to these open market purchases the company makes for paying yield they also purchase an additional 10% CEL to burn every week. If users collectively earned $1 million in CEL one week, Celsius would go to the market and purchase $1.1 million of CEL. They would distribute $1 million to users and burn $0.1 million. This burn mechanic puts additional buying pressure on the token while also reducing the supply. CEL token is burned by sending coins to the 0x0 address.

The DeFi alternatives for the Earn product are staking and yield farming. Users who choose to stake run the risk of being slashed if the entity they delegate their stake to behaves poorly. Yield farming comes with the risk of impermanent loss. There are many more risks users bear when earning yield through decentralized means. For some users the risks of pure DeFi yield solutions are preferable to the risks of earning yield through centralized means like Celsius.

Borrow

Celsius allows users who have assets in the platform to borrow against them. For example, a user can “lock up” some bitcoin stored in their Celsius wallet to get some stablecoins. When a user takes a loan they have to pay interest on what they borrow and the collateral they provide (bitcoin in the above example) no longer earns the user interest. All consumer loans on celsius are overcollateralized. This means that the USD value of the locked coins is higher than the USD value of the loan. The ratio of the loan (or, what’s borrowed by the user) to the value of the assets put as collateral is called the Loan To Value (LTV) ratio. Celsius offers three different LTVs to users: 50%, 33% and 25%. For example, a user might lock up $1000 of bitcoin to borrow $250 of USDC which is an LTV of 25%. Lower LTVs come with lower interest rates. All loans with 25% LTV come with a 1% annual interest rate. In the above example, the user would have to pay $2.5 of interest on their $250 loan if they take the loan for a year. Celsius offers loans as short as 6 months. Celsius offers a loan calculator on their website.

In general taking a loan and paying it off are not considered taxable events (though you should confirm with your accountant). Loans provide a way for users to get cash without giving up ownership of the underlying collateral. For example, a user may choose to take a loan to pay off their credit card because the interest rate for a loan is 1% compared to the 24.99% on a credit card. Then, the user can pay off the Celsius loan and get their collateral back.

Similar to the Earn product where users are incentivized to earn in CEL, users are incentivized to pay interest on loans in CEL. Users who choose to pay their interest in CEL receive discounts based on the relative USD value of their CEL and non-CEL portfolios. The more CEL you have, the lower your interest rate. Users with platinum status pay 25% less in interest over the life of a loan.

Because of the volatility of crypto markets users who take loans may suffer a margin call. Margin calls happen when the price of the collateral falls too much relative to the value of the loan. For example, if a user locks up $1000 of BTC for $250 of USDC (for an LTV of 25%) and then the price of BTC drops by 75% (such that the value of the collateral is now $250) the LTV will be 100%. At this point Celsius risks not having enough assets to cover the loan if the user defaults (ie: the user decides to not repay the loan) so Celsius will issue a margin call which results in the collateral being sold.

Similarly, if the price of the collateral increases the user can request a reverse margin call where Celsius will unlock some portion of the collateral provided for a loan. As an example, suppose the price of BTC in the above example rises by 100% such that the collateral is now worth $2000. Now that the LTV is 12.5% the user can request that some BTC be unlocked by Celsius so that the interest-earning portion of the users portfolio increases (remember that locked collateral doesn’t earn interest). Note that reverse margin calls change the LTV and a subsequent drop in the price of BTC may result in a margin call.

DeFi alternatives to Borrow exist. One big player in the lending space is Aave. Just like yield farming and staking there are risks with pure DeFi lending protocols. One risk is that margin calls are executed through smart contracts which means there isn’t room for human judgement - when certain conditions are met, the margin call is executed algorithmically. There are many examples of the Celsius team giving borrowers more time to meet margin calls. Some users may prefer (and see less risk) in systems that are purely algorithmic and don’t involve human judgement.

Pay

CelPay is extremely similar to PayPal and Venmo except that CelPay is for crypto while PayPal and Venmo are for fiat. CelPay enables users to send crypto to others without having to worry about complex wallet addresses. CelPay allows payments to happen through link sharing and emails already registered with Celsius.

Payments made through CelPay are not settled on the blockchain. They are managed through an internal accounting system of the Celsius. Because of this, they are near instant. Payments made through CelPay are only settled on the blockchain when users withdraw their funds from Celsius. Approximately 75,000 payments have been made through CelPay with an average payment size of $743.

Buy

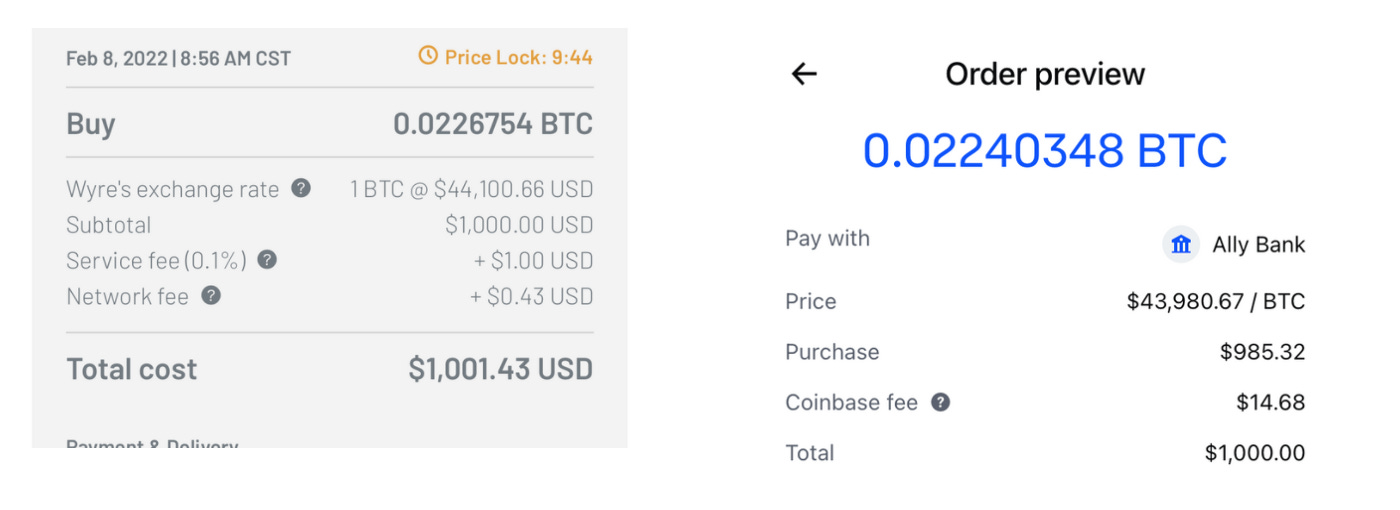

Celsius offers it’s users a mechanism to purchase crypto directly through the app. Celsius partners with Wyre and Gem to power this feature. Celsius boasts fees as low as 0.1% for ACH purchases which is among the lowest in the industry. What Celsius doesn’t make transparent is the spread users have to pay to use this functionality. Still, it seems the the rates offered through Gem and Wyre are still much better than the rates offered by Coinbase.

As of February 2022 Celsius is still building their own fiat on ramps so that they no longer rely on Gem and Wyre. This functionality has been delayed many times. Right now Celsius offers no way to withdraw fiat but once they have their own in house fiat ramps it’s expected users will be able to withdraw fiat to their traditional bank accounts as well.

Swap

Swap is a new product by Celsius which allows users to swap between assets supported by the platform, for example swapping between BTC and ETH or ETH and USDC. Celsius uses Chainlink as a price oracle to determine the relative value of any two assets during a swap. Celsius also offers (near) 0 spread swaps which is the best (or among the best) in the industry. A spread is the difference between the market rate for a transaction and the rate a trader gets through a platform. Coinbase mentions in their documentation that they charge a spread dynamically based on market conditions and other sites mention spreads of 0.5% for Coinbase. In addition to spreads, Coinbase also charges up to 2% in conversion fees when swapping from one coin to another. One user compared purchasing $50 of BTC with USDC got 4.4% more BTC when using Celsius.

The exact details for how and why Celsius can offer 0 spread swaps aren’t clear. One important thing to note is that Celsius has daily limits for how much users can swap. At the time of writing the limit is $10,000 USD per day and there are talks of increasing this to $250,000 USD per day for platinum members. Celsius doesn’t use swaps as a revenue generating mechanism and places limits to ensure there are caps to their infrastructure costs. Contrast that to Coinbase which started as an exchange where their primary revenue generation came from users swapping between assets for a fee. Coinbase still uses trading fees as their primary revenue generating mechanism (as do most other centralized exchanges) and it’s unlikely they will reduce their fees unless they can find new revenue streams.

CelsiusX

CelsiusX is the latest initiative from Celsius. CelsiusX is being marketed as the DeFi arm of Celsius. CelsiusX aims to be bridge between the centralized/traditional finance world and the decentralized finance world. A few initiatives that have been announced from CelsiusX include: wrapped tokens, cross-chain liquidity and actively managed stablecoins. Celsius is partnering with Polygon, Enzyme, and Chainlink as part of this initiative.

CelsiusX hasn’t released detailed information on what each of these initiatives mean, why they’re important, when they will be delivered, how they will accrue value to the CEL token or much of anything else. However, it seems that Celsius now supports asset deposits on Polygon based on user reports of success. It’s reasonable to assume that users will soon be able to withdraw their ERC-20 assets to Polygon as well sometime in the future.

Celsius has announced a partnership with Chainlink and their Proof of Reserve (PoR) protocol to enable wrapped tokens and cross-chain liquidity. This system will initially be used to launch wrapped versions of ADA, DOGE and ETH on Polygon. Enzyme will be used as the vault which holds the native assets and PoR will be used to securely mint wrapped assets on Polygon.

CelsiusX has launched a bug bounty program with ImmuneFi. Celsius will payout up to $1 million for bugs. More details can be found on the ImmuneFi page.

CelsiusX is the fastest moving product in the Celsius ecosystem and I expect the information in this section will very quickly become outdated.

Proof of Community

Proof of Community is an initiative at Celsius to increase transparency of assets in the platform. The main product to come out of this initiative is the rewards explorer which can be found when you sign into the web and mobile apps. The mechanics of the rewards explorer can be found on this page. The rewards explorer displays the total number of users, the total USD value of yield paid to the community, number of active users, total assets in the system, stats on the most popular coin, fees covered by Celsius, stats for CelPay and the stats on the membership tiers (Bronze, Silver, Gold and Platinum). In addition to this realtime dashboard Celsius has also partnered with Horizen for “near-real-time audits” which helps power the Rewards explorer. Centralized competitors to Celsius have yet (to my knowledge) released anything with this level of transparency in near-real-time.

Corporate Products

Corporates can use the Earn, Borrow and Pay (I think) features available to consumers. In addition to the above consumer products, Celsius has been building out corporate and institutional specific offerings. Celsius has built a yield generating API which enables other businesses to offer their customers yield on their crypto. For example, Voyager is a wallet and exchange that uses the Celsius API to provide yield to customers holding assets in Voyager wallets. Similarly, Paxful uses the Celsius API to provide yield to Nigerians who store BTC with Paxful. Celsius has many partnerships and the list continues to grow.

Marketing

Celsius has taken a non-traditional approach to marketing so far. The company has mostly focused on word of mouth marketing with an extremely generous referral program. The referral program started by offering $10 in BTC to both referrers and referees when a new user signs up with a referral code and deposits $400 USD worth of crypto into their Celsius wallet for 30 days. That program has since expanded to giving both participants $50 USD.

Celsius also runs weekly AMAs on YouTube with the CEO. This program started in 2019 and I don’t think a single week has been skipped (though it’s hard to find solid evidence of this).

Celsius hadn’t spent much traditional marketing (like ads) prior to hiring Tushar Nadkarni in November of 2021. Since then Celsius has also hired Jennifer Kattula as VP of Marketing in an effort to build out the global marketing program for the business.

Celsius also posts weekly statistics on asset inflows and outflows on Twitter. For example, the week of January 28th the company saw net inflows of $116 million.

Business Fundamentals

How Earn and Borrow Generate Revenue

Celsius primarily makes money through their Earn and Borrow products. Celsius loans user assets to other institutions such as hedge funds and market makers for a fee, 10% annually for example. Celsius then pays users up to 80% (8% in this example) of the fees they earn while pocketing the difference (2% in this example). Hedge funds are interested in borrowing funds from Celsius in order to take long and short positions on the market in a leveraged way. Market makers, similar to Coinbase and Binance (though not necessarily those two), are interested in borrowing funds because the deeper their markets are the better the trading experience on their platforms. In addition to loaning funds out to institutions Celsius earns fees through yield farming, staking and other DeFi primitives.

Celsius earns even more profit when users decide to borrow against their assets. Remember that when a user locks up some BTC to get a USDC loan (for example) the locked up BTC no longer earns interest for the user. However, Celsius still loans the BTC out to hedge funds and market makers but now keeps all the fees earned on that BTC instead of distributing rewards to the user. On top of that, Celsius also gets revenue from interest payments that users make on their loans.

Bitcoin Mining

Celsius has cumulatively invested $500 million Bitcoin mining, making them one of the largest bitcoin mining operations in North America. Celsius uses the Bitcoin they mine to support the lending business and providing more stable interest rates to users who deposit their assets in the platform. The details of this mining operation are quite sparse though Alex, the CEO, claimed in a recent YouTube AMA that the mining operation is now worth several billion dollars by itself.

Acquisitions

Celsius has made two notable acquisitions to date: GK8 for vertical integration of MPC technology and MVP Workshop as an acquihire. MPC is a technology which enables more secure management of crypto wallets, the exact details of it are outside of the scope of this document. Vertically integrating GK8 will let Celsius add coins and tokens to their platform faster and increase the security posture of Celsius quite significantly since they will be able to enable far deeper security integrations. MVP Workshop worked with Celsius in early days to launch the mobile application and has also worked on other products like Aidonic and Anchor. The acquisition of MVP Workshop significantly enables the web3 engineering of Celsius and should enable the company to release new features and products faster.

Fundraising

Celsius has had 3 fundraising events: an ICO, a Series A and a Series B. The company raised $50 million in their ICO, $20 million in their Series A, and $750 million in their Series B. The Series A was run through BnkToTheFuture which aims to democratize access to private investments in financial technology companies. Approximately 1000 investors participated in the Series A which valued the company at $150 million. The Series B was done through more traditional means with two lead investors: WestCap and CDPQ. The Series B values Celsius at ~$7 billion, approximately 46x more than the Series A. It’s important to note that CDPQ is a large pension fund in Canada. Alex likes to talk about the difficulty of getting an investment from a pension fund because of their very strict due diligence requirements. Alex has mentioned that passing this due diligence bar will help with any regulatory hurdles the company may face in the future because it’s very unlikely that a pension fund this large will take regulatory risk with investments they make. Time will tell if this is true.

Security

Celsius has never been hacked. However, 3rd party service providers of Celsius and DeFi products Celsius uses for yield generation have been hacked. It’s not clear how much Celsius lost in the BadgerDAO hack but Alex claimed in an AMA that the company has started recuperating lost funds and has recovered ~$30 million since. Note that neither of these two hacks were of Celsius itself but of other products Celsius uses.

Celsius uses multi-party computation (MPC) to secure funds which are deposited into the platform but not lent out. MPC is a technology which increases the security of crypto wallets by splitting and geographically distributing private keys. The exact details of MPC are out of the scope of this document. Celsius uses two MPC providers: Fireblocks and GK8. Celsius recently acquired GK8 and Fireblocks recently raised $550 million bringing it’s valuation up to $8 billion. Using 2 MPC providers puts Celsius at the leading edge of security.

Celsius also has insurance for their cold wallets through FireBlocks. The company is also building an internal insurance product which was announced in early 2021. The details of this self-insurance aren’t clear but it will enable users to opt into a Celsius insurance fund in exchange for some yield. For example, users may opt to give up 2% of the yield they earn which will be put into an insurance fund to backstop any losses the company may suffer in the future.

The security team for Celsius has at least 25 people which is larger than the entire team of many DeFi projects according to Alex. Several videos have mentioned how a non-trivial portion of the security team has a background with the Israeli military.

Growth

Celsius has seen significant growth since inception. 2021 was a great year for the company where they saw many of their investments start to pay off. For example, their AUM in January 2021 was ~$5 billion while their AUM in January 2022 was ~$17 billion even though crypto prices are approximately the same (at the time of writing BTC is up 7.8% over the past year). Similarly, the number of users on the platform has increased from ~113k to ~519k.

The company’s valuation grew from ~$150 million to ~$7 billion between 2020 and 2021. Private investors and venture capital are voting with their dollars investing in the company at such a large valuation.

Celsius had a team of approximately 200 in April of 2021 and has since grown to 800+ employees as of January 2022. Even with a 4x employee growth in a matter of months the company still has ~200 open positions.

I’ve tried to find evidence of how many tokens were added to the platform in 2021 but haven’t been successful. My estimate as a user is that ~15 coins/tokens were added in 2021. The company is predicting approximately 50 new tokens will be added in 2022, powered significantly by their acquisition of GK8.

The company has also seen significant growth on the corporate side of the business from API partners to corporate accounts. Again, I can’t find evidence of this though I remember an old AMA claimed ~5000% increase YoY on one of these metrics.

CEL value accrual

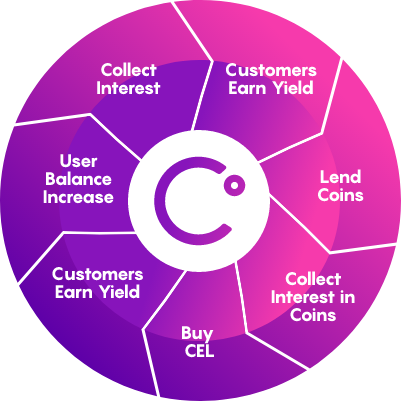

Celsius has implemented a flywheel similar to that of Amazon back in the late 90s and early 2000s. Amazon’s flywheel centered around two self reinforcing loops which Bezos theorized would lead to growth of the company. More sellers means more selection which leads to a better customer experience which leads to more traffic and loops back to more sellers. Similarly, more growth leads to a lower cost structure which leads to lower prices which improves the customer experiences which loops back to more growth. It’s clear the the flywheel of Amazon has been extremely successful.

The Celsius flywheel follows a similar pattern but has 1 loop instead of 2. This flywheel specifically focuses on the value of the CEL token as opposed to generalized growth focus for Amazon.

The more users Celsius can acquire, the more interest they pay out in CEL token. The more interest that gets paid in CEL token the more buying pressure there is which drives the price up, enticing even more users to opt to earn their interest in CEL. Celsius has added several other features to increase the utility of CEL such as higher interest rates for users earning in CEL and lower borrowing rates for users paying off loans in CEL. Celsius has also implemented a buy-and-burn program outlined in greater detail under the Earn heading. This puts additional buying pressure on the token while also reducing the supply, both of which add upward price pressure on the token. This upward price pressure will eventually lead to more users choosing to earn in CEL.

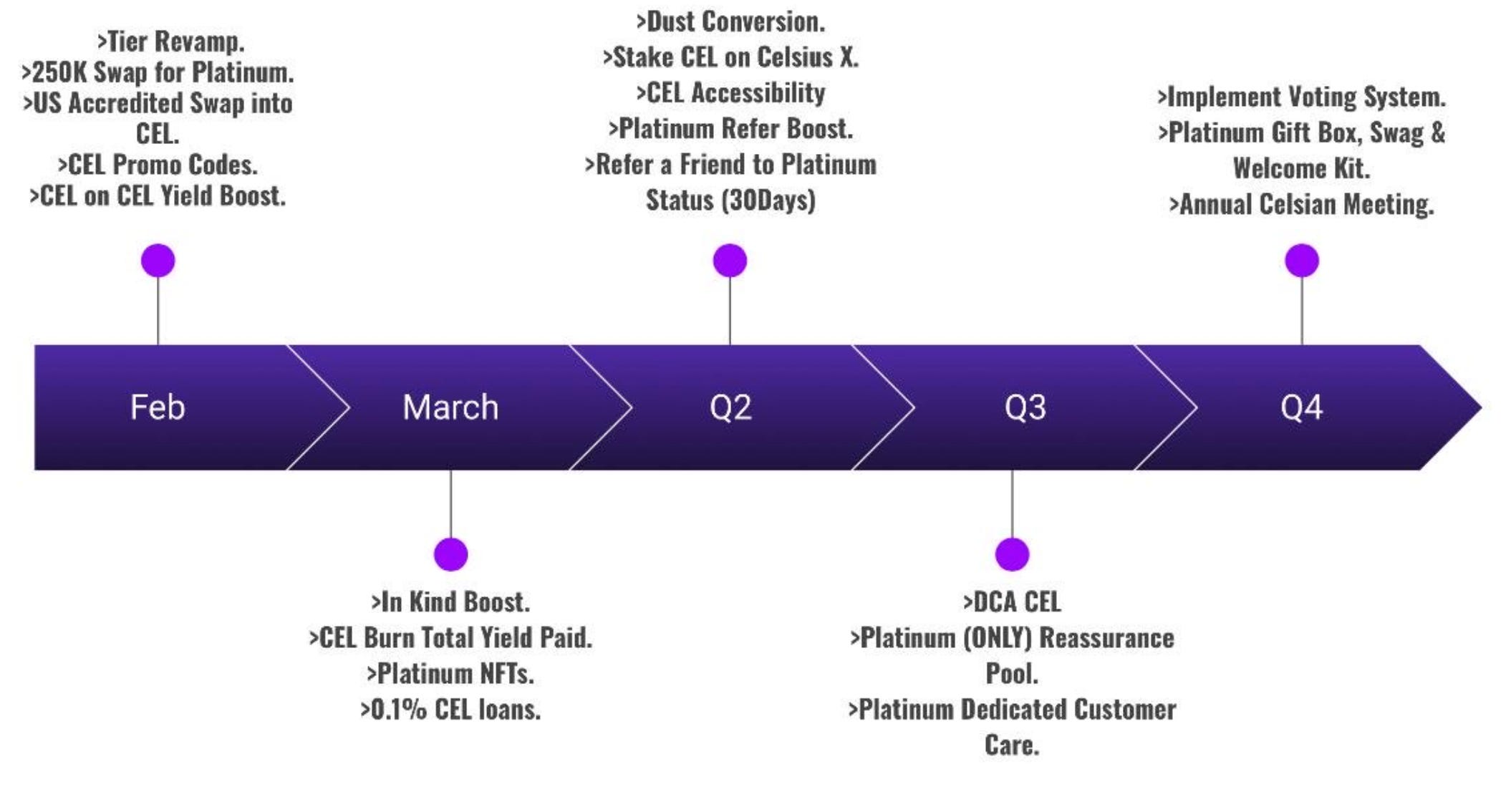

Celsius is working on adding even more utility to the CEL token. The roadmap for adding more utility isn’t very clear though Alex suggested the following roadmap for 2022 in late January.

At a high level, this roadmap provides even greater incentives for users to become Platinum members of Celsius because they would get higher swap limits, better referrals, NFTs, dedicated customer care, a reassurance pool (though it’s not clear what that is) and more. Other incentives will be added and the team has signaled that they have other ideas for how to improve the tokenomics of CEL as well.

Bull Case

There are many reasons to be bullish on Celsius and CEL. The recent fundraising by the company gives them a lot of capital to deploy towards improving the business and launching new products. One initiative we’ve seen since the fundraising is the launch of CelsiusX which is a DeFi play by the company. Because CelsiusX is closer to DeFi than CeFi we may seen much faster product development - fewer regulatory hurdles means less compliance issues which improves product velocity. Celsius has ~800 employees right now and has many job openings, on the order of 200. The company was growing extremely quickly prior to the recent investment round and will now grow even faster.

The tokenomics outlined above are well thought out with a clear value accrual mechanism. In addition to this value accrual mechanism the CEL smart contract has a fixed supply of 7000000000000 without a mechanism to print more CEL. In addition, the company has started a program of burning CEL tokens based on market demand. This makes CEL one of the few deflationary currencies in the ecosystem. Alex posted the following graphic but I haven’t seen it verified in any meaningful way.

Celsius seems to have played nicely with global regulators since inception. This is hard to verify since conversations with regulators are kept private but we can examine actions the company has taken in an effort to be compliant. Celsius didn’t offer US residents (even accredited ones) the option to earn their yield in CEL because of the potential implications of securities rules. In early 2022 the company announced that the regulatory hurdles of earning in CEL in the US have been cleared for accredited investors. However, accredited investors choosing to earn in CEL will have their yield locked for a year for regulatory reasons. In addition to this, the company has earned several licenses such as FinCen MSB and ISO 27001. The actions of the company seem to match their words in regards to their desire to be compliant with all regulations.

Celsius has a history of rolling out products that are best-in-class in addition to being highly compliant with global regulations. For example, Swap gives consumers access to wholesale prices, much cheaper than what is offered at other centralized exchanges. Celsius still has the best yield product in the industry. They have best in class security as evidenced by the fact that they haven’t been hacked (though that doesn’t mean they will never be hacked). It’s reasonable to assume they will continue to deliver high quality products but only time will tell if they can keep a high bar for innovation and product delivery.

The company has also seen incredible growth, especially in AUM and active users. We outlined above more of the growth metrics of the company above and there’s little reason to believe those patterns will be interrupted, especially with the recent fundraising which should enable even greater growth.

Bear Case

All investments carry a risk and Celsius is no different. The beginning of the article outlined many risks of investing in Celsius from a perspective of centralization. If Celsius gets coopted by a government, all credibility in the company might evaporate leaving users and investors with empty hands. These are fairly abstract risks and for many difficult to reason about effectively since there are so many companies which succeed in a centralized environment.

One big criticism of Celsius is their partnership with Tether who was a primary investor in the Celsius Series A. Many people in the industry perceive Tether as a scam. Here’s one write up on the topic - searching will yield many more results. Discussing the details of Tether are out of the scope of this article but it’s something investors/users should be aware of. I personally find the Series B with a large pension fund to be a strong vote of confidence in the face of this Tether controversy (since pension funds are typically very risk averse) but smart investors have been fooled throughout history and now is no exception.

Above I mentioned how the regulatory compliance of Celsius is a reason to be bullish. This is also a reason to be bearish because it significantly slows innovation. The 2010s popularized extremely quick innovation and iteration and much of that philosophy bleeds in the crypto industry. For example, Cardano has famously been extremely slow to market and ruthlessly criticized for it. Celsius is in a similar position. Celsius announced in early 2021 that Swaps would be out soon. The product got delayed many times and once it was released, it was only released to a small subset of users. Some of this delay comes from the technical difficulty of the software but now that the software is finished the reason some users don’t have it is because of jurisdiction. I’ve been a platinum member for over 2 years but Swaps have yet to be released to my country of residence, Canada.

In addition to the delays and issues with Swaps, Celsius has so far failed to deliver their self-insurance and credit card products. These were also announced early in 2021 with quick timelines but no meaningful product development has been shown to the community. Examples of Celsius overestimating their capacity to deliver include Nuke (the CTO) predicting that an early swap product will be ready by May 2021 in mid April 2021. It’s 2022 now and many users still don’t have Swap. A lot of the community (based on sentiment in the Celsius Investor telegram) has lost confidence in Celsius because of these product delays. Similarly, it was predicted in April that Cardano will be added to the platform in May but Cardano was actually added in August. Also in April it was predicted accredited investors in the US will be able to earn in CEL but that wasn’t launched until January 2022.

Celsius burns CEL token on a weekly basis since they launched their burn program around October 2021. The fundamental theory of deflationary tokens isn’t well researched and I’m personally not convinced that this is a good mechanic to introduce. It feels oddly similar to a central bank trying to control the rate of inflation without regard for 2nd and 3rd order consequences. I have not yet found a good explanation of the 2nd and 3rd order consequences of deflationary currencies. The first order consequence of adding a burn mechanic is reduced supply which will add upward price pressure on the token but it’s not clear how this mechanic will work at the limits - what happens when there’s only 1 CEL token left? The company also hasn’t sufficiently justified why a 10% burn is optimal - why not 1%? or 11%? or 99%? Stellar burned 55 billion of their tokens in 2019 and that did not have a significant impact on the price of the coin. Why won’t this happen to Celsius?

Celsius has strong branding around having 0 fees and they do a good job delivering. Swapping is fee free, taking a loan is fee free, closing a loan is fee free, withdrawing is fee free. However, they charge a 3% fee when liquidating a loan. Many members of the Celsius Investor Club telegram group reported this fee during the Jan 2022 sell off (note this is a link to a private group so you will need to get access to the group before you can see this message). The branding around 0 fees while simultaneously charging liquidation fees is a great way for the company to lose the trust of it’s community.

Conclusion

Celsius is quickly becoming one of the most prominent businesses in the crypto world. Since inception in 2017 they have accumulated more than $10 billion in AUM and have paid over $700 million in rewards (though at one point this was a billion but because of the market downturn this number had to be revised). The company has also grown to over 800 employees with more on the way powered by very large investments. The founding team has lots of experience and the community is fairly strong even if the recent market downturn changed sentiment. The business has great fundamentals and continues to diversify and build industry leading products. However, the company is slow to execute and has gone through significant growing pains. The tokenomics of CEL are great and continue to improve as more products are released which integrate the token. CelsiusX is being launched with much faster product velocity than the more traditional arm of the business which can have outsized impact on the quality, revenue and strategic positioning of the company. The bitcoin mining arm of the business is growing in value and is a great diversification strategy for revenue since it does not depend on external entities as much as the lending business. I have a non-trivial allocation in CEL at the time of writing and don’t intend to liquidate my position unless the fundamentals of the business take a turn for the worst.